Most people treat health insurance as a purely defensive financial decision — you pay premiums hoping you never need to use them. But there’s one account that flips this around: the health savings account. An HSA isn’t just a way to pay for medical expenses. When used correctly, it becomes a stealth retirement account with a triple tax advantage that no other financial product can match. If you’re not maximizing this benefit, you’re leaving thousands of dollars on the table every year.

I’ll walk you through what an HSA is, why the tax treatment is so favorable, who qualifies, and how to make the most of it. I’ll show you the numbers, the strategy, and the limitations you need to understand before opening an account.

What Is a Health Savings Account (HSA)?

A health savings account is a tax-advantaged savings account available to individuals who enroll in a high-deductible health plan. Unlike flexible spending accounts, which use a “use it or lose it” structure, HSA funds roll over year after year. There is no expiration date on your contributions, and the money remains yours even if you switch jobs, change insurance plans, or retire.

The account serves two primary functions. First, it provides a tax-favored way to pay for qualified medical expenses — everything from doctor visits and prescriptions to dental work and vision care. Second, it allows you to invest the funds in your account, potentially growing your savings over time.

What makes HSAs unique is their flexibility. You can contribute to an HSA at any point throughout the year, as long as you maintain eligible high-deductible health plan coverage. Unlike employer-sponsored benefits that require open enrollment decisions, you can open an HSA independently through many banks, credit unions, or brokerage firms. This portability means your account travels with you throughout your career, accumulating value regardless of your employment situation.

The accounts gained traction after the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 created them. Since then, contribution limits and eligibility thresholds have increased nearly every year, reflecting their growing role in American financial planning.

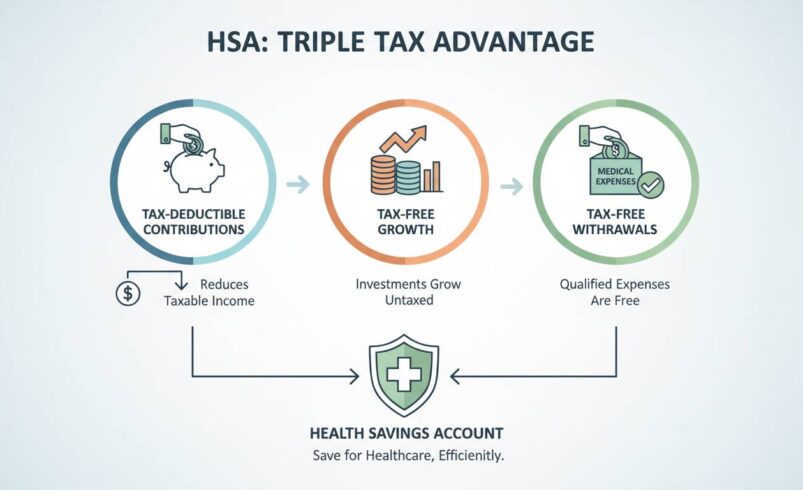

The Triple Tax Advantage Explained

This is where HSAs stand out from other financial products. The tax treatment applies at three distinct stages — contribution, growth, and withdrawal.

Tax-Deductible Contributions

Every dollar you contribute to an HSA reduces your taxable income. For 2025, you can contribute up to $4,300 for individual coverage or $8,550 for family coverage. If you’re 55 or older, you can add an additional $1,000 catch-up contribution. These contributions are above-the-line deductions, meaning you claim them whether you itemize or take the standard deduction.

Here’s what this looks like in practice. Suppose you’re in the 24% federal tax bracket with a family HSA. Contributing the maximum $8,550 reduces your federal tax liability by $2,052. Factor in state income taxes — which in states like California and New York can add another 5-10% — and your actual tax savings could exceed $2,500. That’s real money back from the government, not a theoretical benefit.

Tax-Free Growth

Once money sits in your HSA, it grows tax-free. Unlike a 401(k), which taxes investment gains when you withdraw in retirement, an HSA never taxes your investment gains. This creates exponential growth potential over time.

Your HSA funds can be invested in mutual funds, ETFs, stocks, or bonds — just like a brokerage account. Many HSA providers offer self-directed investment options once your balance reaches a certain threshold, typically $1,000-$2,500. The investment growth compounds without any annual tax drag. Over a 20- or 30-year horizon, this tax-free compounding can transform your HSA into a substantial nest egg.

Tax-Free Withdrawals

When you withdraw HSA funds for qualified medical expenses, the withdrawal is completely tax-free. This includes your original contributions, your employer contributions, and all investment gains. The government never taxes money spent on IRS-approved medical expenses.

This differs fundamentally from a 401(k), where withdrawals are taxed as ordinary income, or a Roth IRA, where you’ve already paid taxes on contributions but withdrawals of earnings are restricted.

The triple advantage is real. No other account offers this complete tax trifecta — deductibility on the way in, tax-free growth in the middle, and tax-free withdrawals on the way out.

HSA vs FSA: What’s the Difference?

This comparison trips up a lot of people, and I understand why. HSAs and FSAs both deal with healthcare costs and sound similar in conversation. But the differences are significant, and choosing wrong can cost you thousands.

A flexible spending account is employer-sponsored. You set aside pre-tax dollars during open enrollment, and you must use that money within the plan year or lose it. While some employers now allow a small carryover (typically $610 for 2024), FSAs fundamentally operate on a use-it-or-lose-it basis. If you contribute $2,850 to an FSA and only spend $1,500, you forfeit $1,350.

An HSA, by contrast, belongs to you. Funds roll over indefinitely. There’s no “use it or lose it” pressure. You decide when to contribute, when to spend, and when to invest. If you change jobs, your HSA comes with you. If you don’t touch it for five years, it’s still there.

FSAs also require you to estimate your annual medical expenses in advance and commit to that contribution amount. HSAs allow much more flexibility — you can contribute up to the annual limit at any point during the year, including after you’ve already incurred expenses.

One thing to consider: FSAs aren’t entirely without value. If you have predictable, recurring medical expenses and you know you’ll spend the money, the FSA still provides the same tax deduction. But for most people building long-term wealth, the HSA wins decisively because of the investment option and rollover feature.

Who Is Eligible for an HSA?

Eligibility isn’t automatic. You must meet two specific requirements to open and contribute to an HSA.

First, you must be covered by a high-deductible health plan. For 2025, an HDHP must have a minimum annual deductible of $1,650 for individual coverage or $3,300 for family coverage. The plan’s out-of-pocket maximum cannot exceed $8,300 for individuals or $16,600 for families. These figures represent increases from 2024’s thresholds ($1,600/$3,200 deductible and $8,050/$16,100 out-of-pocket).

Second, you cannot be claimed as a dependent on someone else’s tax return. This is straightforward for most working adults but worth noting for parents with adult children.

You can have an HSA even if your spouse has different insurance coverage, as long as you maintain eligible HDHP coverage yourself. However, if you’re covered under a spouse’s non-HDHP plan or enrolled in Medicare, you generally cannot contribute to an HSA. These eligibility rules come directly from the IRS, and there are no exceptions.

One nuance worth understanding: you can be eligible to contribute to an HSA even if your employer doesn’t offer one. Individual HSA accounts are available through numerous financial institutions, and you establish eligibility by being enrolled in an HDHP, regardless of where you obtain that insurance.

How Much Can You Contribute?

For 2025, the contribution limits are $4,300 for individuals with self-only HDHP coverage and $8,550 for families with family HDHP coverage. If you turn 55 during the tax year, you become eligible for catch-up contributions of an additional $1,000.

These limits apply to total contributions from all sources — your own deposits, employer contributions, and anyone else’s contributions on your behalf. If both spouses have separate HSAs and each has family HDHP coverage, both can contribute the family maximum, effectively allowing $17,100 in combined contributions for 2025.

The contribution deadline follows the same rule as IRAs — you have until Tax Day (typically April 15) to make contributions for the prior tax year. This gives you a small window after year-end to maximize your previous year’s deduction.

One practical strategy: if you can afford to pay current medical expenses out of pocket and instead invest your HSA contributions, you preserve the tax advantage while building long-term savings. This “pay yourself first” approach works because HSA withdrawals for qualified expenses are tax-free regardless of when you incur them. You can reimburse yourself years later for expenses paid today, as long as you maintained HSA eligibility at the time of the expense.

How to Open an HSA

Opening an HSA is straightforward, but the provider you choose matters significantly for long-term returns.

Start by confirming your HDHP coverage. Your insurance card or plan documents should indicate whether you have a high-deductible health plan. If you’re uncertain, check your plan’s deductible against the IRS minimums — $1,650 for individuals in 2025.

Next, select your HSA provider. You have three main options:

Employer-sponsored HSAs through workplace benefits programs offer convenience — contributions can be deducted directly from your paycheck. However, investment options may be limited, and you may face higher fees.

Banks and credit unions provide straightforward savings accounts with minimal complexity. These work well if you plan to use HSA funds for near-term medical expenses. Many offer interest-bearing accounts, though rates vary.

Brokerage firms like Fidelity, Charles Schwab, or TD Ameritrade provide the broadest investment options and typically lower fees for those with substantial balances. These are ideal if you’re treating your HSA as a long-term investment vehicle.

When evaluating providers, pay attention to three factors: investment minimums required before you can access their full menu of options, fee structures (monthly maintenance fees can erode small balances), and whether they offer the investment products you want.

The actual account opening process takes about 15 minutes online. You’ll need your Social Security number, employer information, and HDHP policy details. Once opened, you can begin contributing immediately.

Common HSA Mistakes to Avoid

After working with hundreds of people on financial planning, I’ve seen the same errors repeat. Here are the pitfalls that cost the most money.

Treating it as a checking account. The biggest mistake is leaving HSA money uninvested in a low-yield savings account. With proper investment, your HSA can grow substantially over decades. If you’re young and healthy, paying current expenses out of pocket while investing HSA funds creates far greater long-term wealth.

Not contributing enough. Many people contribute a token amount rather than maxing out their HSA. If you have the financial capacity, the maximum contribution should be a non-negotiable part of your financial plan, right alongside 401(k) and IRA contributions.

Forgetting about reimbursement. You don’t have to reimburse yourself for medical expenses immediately. Save your receipts and documentation. Years later, you can withdraw HSA funds tax-free for those past expenses. This effectively creates a “tax-free withdrawal” window at any point in the future.

Ignoring investment options. Some HSA providers make investing unnecessarily difficult. Once your balance exceeds $1,000 or $2,000, move those funds into investments. A savings account earning 0.1% interest is hemorrhaging opportunity cost against historical market returns.

Confusing HSA and FSA rules. People occasionally try to use HSA funds for non-medical expenses, forgetting the 20% penalty. Unlike HSAs, FSAs have strict “use it or lose it” rules, but HSAs allow tax-free withdrawals only for medical expenses. Non-medical withdrawals before age 65 trigger income tax plus a 20% penalty.

Frequently Asked Questions

Can I use my HSA for non-medical expenses?

Technically, yes, but it’s expensive. Non-medical withdrawals before age 65 are taxed as ordinary income plus hit with a 20% penalty. After age 65, you pay ordinary income tax but no penalty — essentially treating the HSA like a traditional IRA. This penalty structure exists specifically to encourage using HSA funds for their intended purpose.

What happens to my HSA when I retire?

You retain full ownership of your HSA after leaving employment or retiring. There are no required minimum distributions during your working years, unlike 401(k)s and traditional IRAs. This allows continued tax-free growth. In retirement, you can use HSA funds for Medicare premiums, long-term care services, or any qualified medical expense tax-free.

Can I have both an HSA and an FSA?

Generally, no. You cannot contribute to an HSA if you have general FSA coverage, because FSAs are considered other health coverage that disqualifies HSA eligibility. However, some limited-purpose FSAs covering only dental, vision, or specific preventive care may allow HSA eligibility — check with your benefits administrator.

Conclusion

The health savings account is one of the most powerful financial tools available to Americans with high-deductible health plans. The triple tax advantage alone makes it worth maxing out, but the investment growth potential and portability add even more value. This isn’t a fringe strategy or a loophole — it’s deliberately designed tax policy that happens to benefit those who understand how to use it.

The real opportunity lies in thinking beyond immediate medical expenses. If you’re healthy, young, and have some financial flexibility, treating your HSA as a long-term investment account rather than a spending vehicle can generate substantial wealth over your lifetime. The tax-free growth is difficult to match anywhere else.

One honest consideration: HSAs aren’t for everyone. If you struggle to afford the higher deductibles that come with HDHPs, or if you have predictable medical needs that make a lower-deductible plan more cost-effective, the HSA math changes. Run the numbers for your specific situation before committing. The tax advantages are remarkable — but only when they actually apply to your circumstances.