If you’re starting to build an investment portfolio, you’ve likely encountered two of the most common investment vehicles: exchange-traded funds (ETFs) and mutual funds. Both allow you to invest in a diversified collection of securities with a single purchase, but the similarities largely end there. Understanding how these instruments differ will help you make informed decisions about where to put your money.

The distinctions between ETFs and mutual funds affect everything from how much you pay in fees to when you can buy and sell them. These differences matter especially if you’re investing through a taxable account, if you’re working with a limited initial investment, or if you want precise control over when your trades execute. This guide breaks down what each product offers, how they compare across the factors that matter most, and which one might better suit your situation.

What Is an ETF?

An exchange-traded fund (ETF) is a pooled investment that trades on a stock exchange throughout the trading day, just like individual company shares. When you buy an ETF, you’re purchasing a small slice of a portfolio that could contain hundreds or thousands of stocks, bonds, or other assets.

The first modern ETF launched in 1993 when State Street introduced the SPDR S&P 500 ETF (ticker: SPY). This product changed how individual investors could get broad market exposure. Instead of buying each stock in the S&P 500 individually—requiring significant capital and ongoing management—you could buy one security that tracked the entire index.

Most ETFs are passively managed, meaning they simply replicate the performance of a specific index like the S&P 500, Nasdaq-100, or a Treasury bond index. These passive ETFs typically have very low expense ratios because there’s no portfolio manager making active buy-sell decisions. Actively managed ETFs also exist, where a manager trades the portfolio to try to outperform a benchmark, but they generally carry higher fees than passive options.

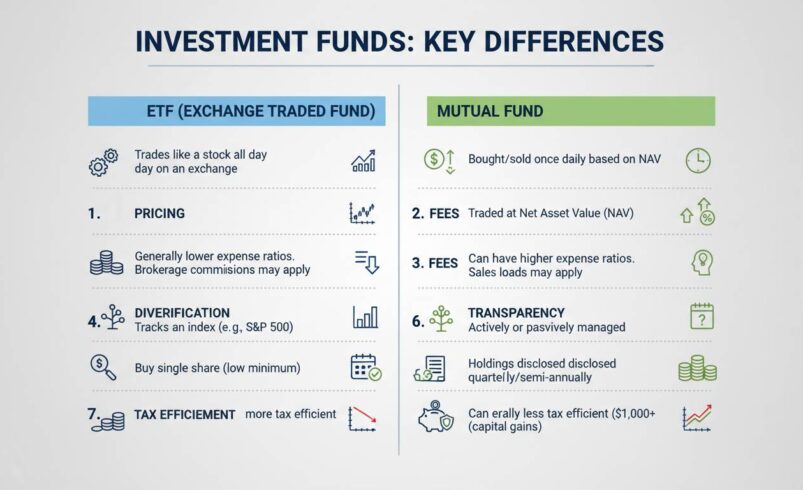

The price of an ETF fluctuates throughout the trading day as buyers and sellers trade shares with each other. This is fundamentally different from mutual funds, which price only once per day. ETF prices can sometimes trade at small premiums or discounts to their underlying net asset value, though this gap is typically narrow and short-lived for heavily traded funds.

What Is a Mutual Fund?

A mutual fund is also a pooled investment, but it operates differently from an ETF in several important respects. When you invest in a mutual fund, you’re pooling your money with other investors, and that money is managed by a professional portfolio manager (or a team of managers) who makes investment decisions on behalf of the fund.

Mutual funds can be actively or passively managed. Actively managed funds employ professional managers who research securities, select investments, and trade to try to outperform a benchmark index. This active management comes at a cost—actively managed mutual funds typically have higher expense ratios than passively managed ones. Passively managed mutual funds, sometimes called index funds, simply track a specific index and have lower fees, similar to passive ETFs.

The most significant practical difference for many investors is how mutual funds are priced and traded. Mutual funds calculate their net asset value (NAV) only once per day, typically after the market closes at 4 PM Eastern time. Every investor who submits a buy or sell order before that deadline receives the same end-of-day price, regardless of when during the day they placed the order. This contrasts sharply with ETFs, which can be traded at any point during market hours at whatever price prevails at that moment.

Mutual funds also historically came with minimum investment requirements. While many fund companies have reduced or eliminated these minimums, some still require $1,000, $3,000, or more to open an account. This barrier has diminished significantly in recent years as the industry evolved.

ETF vs Mutual Fund: Key Differences

Understanding the practical differences between these two investment types will help you choose the right tool for your portfolio. Here’s how they compare across the factors that most directly impact your investing experience.

Trading and Liquidity

ETFs trade on exchanges throughout the trading day. You can place market orders, limit orders, stop orders, and use other trading strategies just as you would with individual stocks. This means you can react to price movements during the day, set precise entry and exit points, and see exactly what price you’re getting at the moment of execution.

Mutual funds offer no such flexibility. Because they price only once daily, you cannot place limit orders or react to same-day news in real time. If the market rallies sharply after you submit your order but before the close, you’ll pay the higher closing price. Conversely, if the market drops, you’ll benefit from the lower closing price. Many investors find this simplicity appealing—it removes the temptation (or ability) to time the market, which most research shows rarely works out well.

Minimum Investments

ETFs have a distinct advantage here: there’s no minimum investment beyond the price of a single share (plus any broker commission). If an ETF trades at $50 per share, you can invest $50. This makes ETFs accessible to investors just starting out or those who want to invest small amounts regularly.

Mutual funds historically required substantially higher minimums, though this has changed. Many mutual fund companies now offer no-minimum versions of their popular funds, particularly for retirement accounts. However, if you’re investing in a mutual fund with a traditional minimum, you might need $500, $1,000, or more to get started. For investors who want to dollar-cost average with very small amounts, ETFs generally win this category.

Expense Ratios

This is where ETFs, particularly passive ones, often have a meaningful cost advantage. The average expense ratio for a passive equity ETF is approximately 0.03% to 0.25%, meaning you pay roughly $0.30 to $2.50 annually for every $1,000 invested. Some of the largest and most popular ETFs charge as little as 0.03%—that’s $0.30 per year on a $1,000 investment.

Mutual funds, especially actively managed ones, typically charge significantly more. The average actively managed equity mutual fund charges around 0.70% to 1.00% annually, though some specialty funds charge 2% or more. Even passive index mutual funds usually cost more than comparable ETFs—often 0.05% to 0.20%. The difference might seem small, but over decades of compounding, even a 0.5% annual fee difference can cost you tens of thousands of dollars on a $500,000 portfolio.

It’s worth noting that not all ETFs are cheaper than all mutual funds. Some specialty ETFs (leveraged funds, inverse funds, actively managed ETFs) can carry expense ratios of 1% or more. And some mutual fund companies have reduced their fees substantially in response to ETF competition. But as a general rule, ETFs tend to be the lower-cost option.

Tax Efficiency

ETFs generally have a significant tax advantage over mutual funds, particularly in taxable brokerage accounts. This stems from how they’re structured and traded.

When you sell an ETF share on an exchange, you’re selling to another investor—the fund itself doesn’t have to sell underlying securities to meet your redemption. This “in-kind” creation and redemption process used by most ETFs means they’re extremely efficient at minimizing capital gains distributions to shareholders.

Mutual funds, by contrast, must sell securities whenever investors redeem shares. If those sales result in profits, the fund must distribute capital gains to all shareholders, including those who didn’t sell. Even if you held your mutual fund shares for years, you might receive a tax bill because other investors sold. This is particularly problematic in years when the fund experiences high redemption activity or when it has accumulated substantial capital gains.

For investors holding these vehicles in tax-advantaged accounts like IRAs or 401(k)s, this difference matters less since taxes aren’t a concern in those accounts. But in taxable accounts, ETFs’ tax efficiency is a meaningful advantage that compounds over time.

Transparency

ETFs disclose their full holdings daily. If you own an S&P 500 ETF, you can see exactly which 500 stocks are in the fund and in what quantities—typically with a one-day lag. This transparency lets you know precisely what you’re invested in and how the fund might be affected by developments in specific companies or sectors.

Mutual funds are far less transparent. Actively managed mutual funds typically disclose their holdings only quarterly, with a significant lag—sometimes 30 days or more after quarter-end. During that window, the manager could have substantially changed the portfolio. Even index mutual funds often only disclose holdings daily or weekly, not in real time. For investors who want to know exactly what they own, ETFs provide clearer information.

Investment Minimums and Automatic Investing

Both ETFs and mutual funds can be purchased through automatic investment plans, which is a smart way to implement dollar-cost investing. Many brokerages offer automatic purchases of both vehicle types on a scheduled basis.

However, because ETFs must be purchased in whole share quantities, setting up automatic investments can be slightly less straightforward. If you want to invest $500 monthly and an ETF trades at $75, you can buy six shares ($450) with $50 left uninvested or cash sitting idle until you accumulate enough to buy another share. Some brokerages address this with fractional share trading for ETFs, but it’s not universal.

Mutual funds were designed with automatic investing in mind. You can typically set up a plan to invest a specific dollar amount monthly without worrying about share quantities—the fund simply invests whatever amount you specify at the daily NAV.

Which Is Better for You?

The answer depends on your specific circumstances, priorities, and account type. Here’s how to think about which vehicle makes more sense for different investor profiles.

If you’re just starting out with limited capital, ETFs’ lack of minimum investment requirements makes them the more accessible choice. You can begin with $25 or $50 and add small amounts over time without facing structural barriers.

If tax efficiency is a priority, particularly in a taxable brokerage account, ETFs generally have the edge. The capital gains distribution issue can be substantial in years with market volatility or high investor turnover in a fund.

If you want intraday trading flexibility and the ability to set precise limit orders, ETFs are the clear winner. This matters less for long-term buy-and-hold investors but can be valuable for those using more active strategies.

If you want professional management and are willing to pay for it, some actively managed mutual funds offer approaches that have demonstrated consistency over decades. Finding those managers, however, is notoriously difficult—most active funds underperform their benchmarks over time.

If you’re investing in a retirement account like a 401(k) or IRA, the tax-efficiency advantage of ETFs largely disappears since these accounts have tax protections anyway. In these accounts, your decision might come down to preference, available funds, and whether your employer plan offers the specific vehicles you want.

If you want simplicity and prefer knowing you’ll execute at the day’s closing price without watching intraday movements, mutual funds offer a more streamlined experience. There’s something to be said for removing the temptation to check prices constantly.

Here’s an honest acknowledgment: for most long-term investors, the difference between choosing an ETF and a mutual fund is smaller than the difference between investing consistently versus not investing at all. Both vehicles can serve you well if you hold a diversified portfolio, keep costs low, and stay invested through market ups and downs. The best choice is the one you’ll actually stick with.

Frequently Asked Questions

What is an ETF and how does it work?

An exchange-traded fund (ETF) is a pooled investment that holds a collection of securities—stocks, bonds, commodities, or combinations—and trades on a stock exchange throughout the day like an individual stock. When you buy an ETF, you own shares of the fund, which represents a proportional ownership in all the underlying assets. Most ETFs track an index (like the S&P 500), meaning they hold the same securities in roughly the same proportions as that index.

What are the main differences between ETF and mutual fund?

The primary differences involve trading flexibility, pricing, costs, and tax treatment. ETFs trade throughout the day on exchanges and price continuously; mutual funds price only once daily at the close. ETFs generally have lower expense ratios, particularly for passive strategies. ETFs are typically more tax-efficient in taxable accounts due to their structure. Mutual funds, especially active ones, offer professional management but usually at higher costs.

Are ETFs better than mutual funds?

“Better” depends on your specific situation. For most investors in most situations, low-cost ETFs are the more efficient choice because of their lower fees, tax efficiency, and trading flexibility. However, some investors may prefer mutual funds for features like easier automatic investing, access to certain actively managed strategies, or the simplicity of once-daily pricing. Both can be appropriate components of a well-structured portfolio.

Conclusion

The choice between ETFs and mutual funds isn’t about finding the objectively superior product—it’s about understanding how each works and selecting the tool that fits your particular situation. For many investors, especially those building taxable accounts or starting with modest sums, ETFs offer meaningful advantages in cost and flexibility. For others, particularly those who value professional management or prefer the simplicity of end-of-day pricing, mutual funds remain a viable option.

What matters most isn’t which vehicle you choose, but that you invest consistently, keep costs low, and maintain a diversified approach aligned with your long-term goals. Both ETFs and mutual funds can serve as excellent foundations for a portfolio when used thoughtfully. The best investor is one who understands what they’re holding and why.