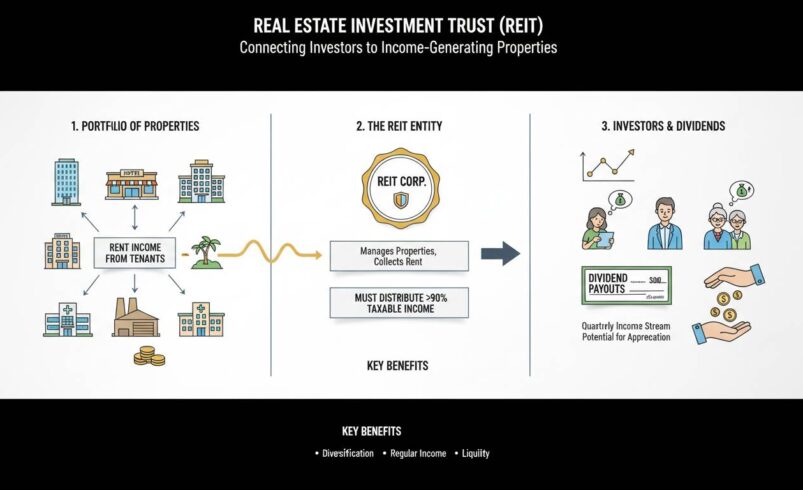

A REIT — short for Real Estate Investment Trust — is a company that owns, operates, or finances income-producing real estate. Unlike traditional real estate ownership where you’d buy property directly, investing in a REIT gives you exposure to real estate markets through shares of a publicly traded company. Congress created the structure in 1960 to let everyday investors access large-scale real estate investments that were previously available only to institutions and wealthy individuals. REITs must distribute at least 90% of their taxable income to shareholders as dividends, which is why they’ve become one of the most reliable income-generating vehicles in the investment landscape.

What is a REIT?

A REIT is a corporation or business trust that invests in real estate assets. The legal definition, established by the Internal Revenue Code, requires that a REIT hold at least 75% of its total assets in real estate, cash, or U.S. Treasuries, and derive at least 75% of its gross income from rents, mortgage interest, or gains from real estate sales.

The 90% distribution rule is what makes REITs distinctive as income investments. A REIT must pay out at least 90% of its taxable income as dividends to maintain its pass-through tax status. This requirement is non-negotiable — fail to comply, and the entity loses its REIT qualification and faces corporate taxation. For investors, this means the structure prioritizes dividend payments above reinvestment or capital preservation in ways that most corporations do not.

There are three primary requirements a company must meet to qualify as a REIT. First, it must be organized as a corporation, trust, or association that would be taxable as a regular corporation but for the REIT election. Second, it must be managed by a board of directors or trustees. Third, its shares must be transferable — this is why most REIT shares trade on major exchanges like the NYSE and NASDAQ, providing the liquidity that direct real estate ownership cannot match.

The practical result: when you buy shares in a REIT like Prologis (PLD), which owns logistics warehouses, or Public Storage (PSA), which operates self-storage facilities, you are indirectly owning the underlying real estate. The rental income these properties generate flows through to you as a shareholder in the form of dividends.

How do REIT dividends work?

REIT dividends work differently than the dividends you might receive from a technology company or bank. Because REITs are required to distribute the vast majority of their income, the dividend yield tends to be higher than average — often between 3% and 8% annually, depending on the specific REIT and market conditions.

The mechanics are straightforward: each quarter, a REIT calculates its taxable income, which includes rental income from properties, interest from mortgage loans, and any gains from property sales. After covering operating expenses, the REIT distributes at least 90% of remaining income to shareholders. These distributions are paid monthly or quarterly, depending on the REIT’s policy.

One important distinction that trips up newer investors is the relationship between funds from operations (FFO) and distributions. FFO is the industry-standard metric for REIT earnings because it adds back depreciation and excludes gains from property sales, giving a clearer picture of operational performance. Many REITs actually distribute more than their FFO, funded partially by borrowing or asset sales. This is not inherently problematic — it’s simply how the 90% rule interacts with the accounting treatment of real estate, where depreciation can significantly reduce reported earnings even when cash flow remains strong.

Adjusted Funds from Operations (AFFO) is a more conservative measure that subtracts recurring capital expenditures from FFO, providing a better sense of sustainable distribution capacity. Savvy REIT investors look at AFFO coverage ratios — whether the REIT is distributing less than it earns in AFFO — as a sign of dividend sustainability.

As of early 2025, REIT dividend yields remain attractive relative to fixed-income alternatives. The Vanguard Real Estate ETF (VNQ), which holds a diversified portfolio of REITs, yields approximately 3.5% to 4%, significantly higher than the 10-year Treasury yield that has fluctuated between 3.5% and 5% in recent years.

Types of REITs

Not all REITs are created equal. The type of real estate a REIT owns — and how it generates income — fundamentally affects your risk profile and expected returns. Understanding the three main categories is essential before investing.

Equity REITs own and operate income-producing real estate. They generate revenue primarily through collecting rent from tenants. This is the most common type of REIT, encompassing office buildings, apartment complexes, retail malls, warehouses, and data centers. When you hear someone talk about investing in REITs for dividend income, they’re typically referring to equity REITs. These companies benefit from both the rental income and potential appreciation in property values over time.

Mortgage REITs (also called mREITs) do not own physical properties. Instead, they finance real estate by originating mortgages or purchasing mortgage-backed securities. Their income comes from the interest spread between what they earn on their mortgage investments and what they pay to fund those investments. Mortgage REITs tend to be more sensitive to interest rate changes than equity REITs — they often borrow at short-term rates and lend at long-term rates, meaning rising rates can compress their profit margins. The yields on mortgage REITs can be substantially higher, sometimes exceeding 10%, but the risk profile is notably different.

Hybrid REITs combine elements of both equity and mortgage REITs, holding both physical properties and mortgage investments. This structure provides some diversification within the REIT allocation itself, though the hybrid category represents a smaller portion of the total REIT market.

Within each category, further specialization exists. Healthcare REITs own hospitals, medical offices, and senior living facilities. Industrial REITs focus on warehouses and distribution centers — a category that has grown dramatically due to e-commerce expansion. Data center REITs operate the facilities that house servers and computing infrastructure. Each sub-category carries its own dynamics, tenant profiles, and risk factors.

REIT dividend tax treatment

The tax treatment of REIT dividends is one area where investors frequently encounter confusion. REIT dividends are generally taxed as ordinary income, meaning they are subject to your marginal income tax rate. This differs from the qualified dividends paid by most domestic corporations, which receive preferential capital gains tax rates.

For the 2024 and 2025 tax years, qualified dividends are taxed at 0%, 15%, or 20% depending on your taxable income. REIT ordinary dividends do not qualify for this treatment. If you hold REIT shares in a tax-advantaged account like an IRA or 401(k), the dividends are deferred or tax-exempt, just like any other investment. In a taxable brokerage account, however, REIT dividends will hit your ordinary income rate.

There is an exception worth knowing: the REIT may designate a portion of its distribution as qualified dividend income if it meets certain requirements related to holding periods and the composition of its income. Some REITs do this, reducing the tax burden for shareholders in higher tax brackets. However, the majority of REIT dividends are taxed as ordinary income, and you should plan your investment strategy accordingly.

This tax treatment is a meaningful consideration when comparing REITs to dividend-paying stocks. A stock like Johnson & Johnson might pay a similar yield but with more favorable tax treatment on its dividends. The REIT’s tax inefficiency is partially offset by the requirement that REITs pay out such a high percentage of income — you’re receiving most of the pre-tax earnings directly rather than having them retained by the corporation.

Popular REITs to know

Several REITs have become household names in the investment community, and understanding what they do provides concrete context for how these companies operate.

Prologis (PLD) is the largest publicly traded logistics REIT globally, with a portfolio of warehouses and distribution centers spanning four continents. The company benefits from the structural shift toward e-commerce, as retailers and logistics companies require more warehouse space. Prologis has historically traded at a premium to its net asset value due to its high-quality portfolio and investment-grade balance sheet.

Digital Realty Trust (DLR) specializes in data centers, providing the physical infrastructure that houses servers and supports cloud computing. As data generation continues to grow exponentially, data center REITs have become increasingly important. Digital Realty operates globally and serves a diverse tenant base including cloud providers, enterprises, and government entities.

Public Storage (PSA) is the largest operator of self-storage facilities in the United States. The business model is relatively straightforward: the company owns storage facilities and rents space to individuals and businesses. Storage demand has proven resilient because it serves an essential need during life transitions like moving, downsizing, or renovating.

Simon Property Group (SPG) owns and operates shopping malls and outlet centers, making it one of the largest retail REITs. The company faced significant headwinds during the retail apocalypse and the pandemic, but has rebounded as it diversified into mixed-use developments and entertainment destinations.

Realty Income (O) distinguishes itself by paying monthly dividends rather than quarterly, which income-focused investors often find appealing. The company owns a broad portfolio of commercial properties across multiple sectors, with long-term net lease agreements that provide predictable income.

These are just examples, not recommendations. Each REIT carries specific risks related to its property types, geographic concentration, and tenant mix.

Risks of investing in REITs

No investment discussion is complete without addressing what can go wrong. REITs face several distinct risks that every investor should understand before allocating capital.

Interest rate risk affects REITs in multiple ways. When interest rates rise, REIT yields become less attractive relative to bonds, putting downward pressure on share prices. For mortgage REITs specifically, rising rates can compress the spread between their funding costs and investment returns. For equity REITs, higher rates increase borrowing costs and can slow property value appreciation. The sensitivity is real — REIT share prices and bond yields often move in opposite directions.

Economic cyclicality means that REIT performance tracks the broader economy. During recessions, tenants may fail to pay rent, occupancy rates may decline, and property values may fall. Office REITs have experienced particular pain since 2020 as remote work reduced demand for commercial office space. The sector continues to grapple with this structural challenge.

Liquidity risk exists because while REIT shares trade on exchanges, the underlying real estate is illiquid. If a REIT needs to sell properties to fund operations or meet obligations, it may be forced to accept below-market prices, particularly in distressed market conditions. This mismatch between the liquidity of shares and the underlying assets is a structural consideration.

Concentration risk deserves attention. Some REITs have significant exposure to a single property, a single tenant, or a single geography. When an anchor tenant like a major retailer or healthcare system leaves, the impact on that REIT’s income can be severe. Diversification across multiple REITs or through a REIT-focused ETF mitigates this risk.

Here’s an honest limitation: predicting which REIT sectors will outperform is notoriously difficult. The best-performing REIT categories shift over time based on macro factors — interest rates, economic growth, technology trends — that are hard to forecast consistently. Unlike evaluating a company’s competitive position, where fundamental analysis provides meaningful insight, timing REIT allocations based on sector forecasts has proven unreliable.

How REITs compare to other dividend investments

Understanding where REITs fit alongside other dividend-paying investments helps clarify their role in a portfolio.

Compared to dividend-growth stocks, REITs typically offer higher current yields but lower dividend growth. A company like Apple or Microsoft pays a lower yield but has consistently raised its dividend for years. REITs, constrained by the 90% distribution requirement, have less capacity to retain earnings for growth, though some do reinvest through property acquisitions and development.

Compared to bonds, REIT dividends are not fixed and can be cut if property performance declines. However, REITs have historically maintained dividends through multiple economic cycles better than many corporate bonds. During the 2008 financial crisis, while bond defaults surged, most equity REITs continued paying dividends — sometimes by reducing capital expenditures or taking on debt, but the income stream persisted.

Compared to direct real estate ownership, REITs provide superior liquidity, lower capital requirements, and instant diversification. Owning a single rental property concentrates your exposure to one property, one location, and one tenant base. A diversified REIT portfolio spreads this risk across hundreds or thousands of properties.

The honest assessment is that REITs serve a specific purpose: generating reliable, above-average income from real estate exposure without the operational headaches of direct ownership. They are not a complete substitute for growth-oriented investments, but they fill an important role in income-focused portfolios.

Building a position in REITs

For investors deciding how to incorporate REITs into their strategy, several practical considerations apply.

If you want broad real estate exposure without analyzing individual REITs, a diversified REIT ETF like Vanguard Real Estate ETF (VNQ) or iShares Cohen & Steers REIT ETF (IYR) provides instant diversification across property types and geographies. The expense ratios are low, typically under 0.15%, and the dividends are passed through to shareholders.

If you prefer individual REITs, the analysis mirrors stock picking: evaluate the quality and location of the underlying properties, the tenant lease expirations, the REIT’s debt levels and interest rate exposure, and the management team’s track record. Pay particular attention to the dividend sustainability metrics — AFFO coverage ratios above 1.0 indicate the REIT is distributing less than it earns, providing a cushion.

Position sizing matters. Real estate is a distinct asset class with its own risk and return characteristics. Many financial advisors suggest allocating 5% to 15% of a diversified portfolio to REITs, though the appropriate amount depends on your income needs, risk tolerance, and overall portfolio construction.

The tax treatment of REIT dividends, as outlined earlier, suggests that holding REITs in tax-advantaged accounts is generally more efficient than holding them in taxable accounts, unless the REIT has designated a significant portion of its distribution as qualified dividend income.

The bottom line

REITs occupy a unique position in the investment landscape: they are required by law to distribute most of their income, creating a structure that prioritizes shareholder returns in ways that other corporations do not. This makes them particularly valuable for investors seeking regular income from real estate without the complications of direct ownership.

The 90% distribution rule is the defining feature, but understanding what drives REIT performance — occupancy rates, rent growth, interest rates, and property values — matters just as much as the dividend mechanics. REITs are not risk-free, and the interest rate sensitivity that has characterized recent years is a reminder that even reliable dividends come with volatility.

What remains genuinely uncertain is how structural changes in real estate — the ongoing evolution of office space demand, the growth of remote work, and the expansion of industrial and data infrastructure — will reshape which REIT sectors deliver the best returns over the next decade. The income will likely continue, but the source of that income may look different. For now, REITs remain one of the most direct paths to earning income from real estate markets, and understanding how the dividend mechanism works is the first step in evaluating whether they belong in your portfolio.