The investing world often feels dominated by stock market drama—the viral tweets about hot tech stocks, the breathless coverage of market rallies and crashes, the endless debate about which company will be the next trillion-dollar giant. But there’s an entire asset class that powers much of the global financial system while flying under the radar of everyday investors: bonds.

If you’ve never owned a bond, you’re not alone. Most beginner investors rush toward stocks, attracted by the potential for higher returns and the excitement of building equity in companies. Bonds, by contrast, feel boring. They’re what your grandparents talked about—steady, predictable, unremarkable. Yet pension funds and sovereign wealth funds allocate significant portions of their portfolios to bonds. There’s a reason for that, and it’s worth understanding before you decide whether bonds deserve a place in your own investment strategy.

This guide covers everything a beginning investor needs to know about bonds: what they are, how they work, the different types available, and whether they make sense for your specific financial situation. I’ll be straightforward about both the advantages and the limitations, because bonds aren’t right for everyone—and pretending otherwise would do you a disservice.

What Is a Bond? A Plain English Definition

A bond is essentially a loan. When you buy a bond, you’re lending money to an entity—typically a government, municipality, or corporation—in exchange for regular interest payments and the return of your principal when the bond reaches its maturity date.

Think of it like this: imagine your local city government needs to fund the construction of a new bridge. Instead of raising taxes to cover the $50 million cost, the city issues bonds. Individual investors—anyone from a retiree to a college fund—can purchase these bonds, effectively lending the city money. The city pays bondholders interest twice a year (this is called the “coupon”), and promises to repay the full amount borrowed (the “face value” or “par value”) on a specific future date.

The entities that issue bonds are called “borrowers” or “issuers.” You, as the bond purchaser, are the “lender” or “investor.” What you receive in return for your money is a contractual obligation from the issuer to pay you back with interest.

This is fundamentally different from owning a stock. When you buy stock, you own a piece of the company—you’re a shareholder, entitled to a share of profits and a vote in corporate decisions. When you buy a bond, you’re a creditor. You don’t own any part of the issuer; you simply have a claim on their cash flows. If the company goes bankrupt, bondholders get paid before shareholders, which is why bonds are generally considered less risky than stocks.

The U.S. bond market is larger than the stock market by total value outstanding, though daily trading volume is lower. This tells you something important: bonds are the backbone of global finance, even if individual investors rarely think about them.

How Do Bonds Work? Understanding the Key Terms

To evaluate whether bonds make sense for your portfolio, you need to understand a few core concepts that determine how bonds are priced and how they perform.

Face Value (Par Value) is the amount the bond will be worth when it matures—this is also the amount the issuer promises to repay you. Most bonds have a face value of $1,000, though some municipal bonds start at $5,000 or higher. When people refer to a bond’s “price,” they often mean whether it’s trading above or below this face value.

Coupon Rate is the interest rate the bond pays, expressed as a percentage of the face value. If you have a bond with a $1,000 face value and a 5% coupon rate, you’ll receive $50 per year in interest (usually paid in two $25 installments). This is why bonds are called “fixed-income” securities—the income you receive is set when you buy the bond and doesn’t change.

Maturity Date is when the bond expires and the issuer repays the face value. Bonds can mature in as little as one year (these are called “short-term” or “notes”) or as long as 30 years (long-term “bonds”). Some government bonds even extend to 50 or 100 years. The maturity matters because longer-term bonds are generally more sensitive to interest rate changes, which I’ll explain in the risks section.

Yield is your actual return on investment, expressed as a percentage. This gets more complicated than it sounds because yield and coupon rate aren’t always the same. If you buy a bond at a discount—say, for $950 when the face value is $1,000—your yield will be higher than the coupon rate because you’re getting the same $50 annual payment on a smaller investment. Conversely, if you pay a premium, your yield will be lower. The current yield also changes as bond prices fluctuate in the market.

Yield to Maturity (YTM) is a more comprehensive calculation that factors in your total return if you hold the bond until it matures, including the difference between what you paid and the face value, and assuming you reinvest all coupon payments at the same rate. This is the number financial professionals usually reference when discussing bond returns, though it’s an estimate that assumes certain conditions hold.

Here’s a concrete example to tie this together: Suppose you buy a corporate bond with a face value of $1,000, a 6% coupon rate, and a 10-year maturity. You pay $1,000 (the bond is selling at “par”). Every year, you receive $60 in interest. At the end of 10 years, you get your $1,000 back. Your total return is 6% per year—the coupon rate, since you bought at par.

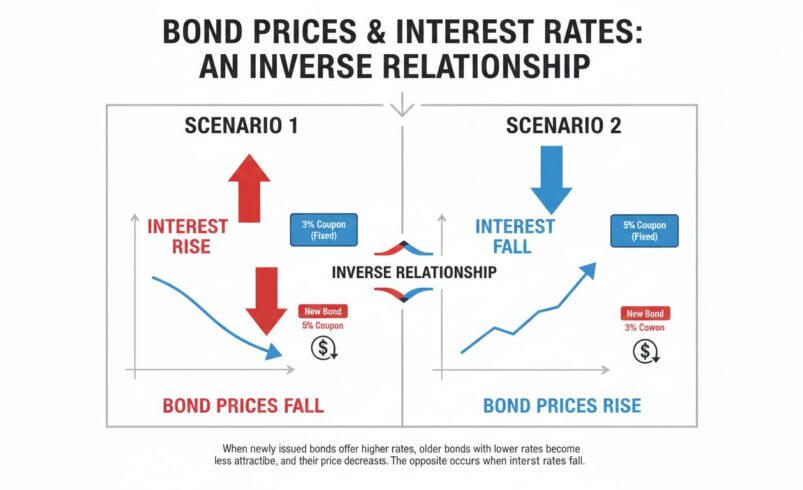

But what if interest rates rise after you buy the bond? New bonds issued after yours might offer 7% or 8%. Your bond becomes less valuable in the secondary market because investors can get better returns elsewhere. If you tried to sell your bond before maturity, you’d likely have to accept less than $1,000. This is the fundamental risk of bond investing, and it’s why understanding yield rather than just coupon rate matters.

Types of Bonds Every Beginner Should Know

Not all bonds are created equal. The issuer, the tax treatment, and the structure all affect what you can expect to earn and what risks you’re taking on. Here are the main categories:

U.S. Treasury Bonds are issued by the federal government and are considered among the safest investments in the world—some would argue the safest, since the U.S. government has never defaulted on its debt. Treasury bonds are backed by the full faith and credit of the U.S. government, meaning the Treasury can technically always print money to meet its obligations.

There are several subtypes within this category:

- Treasury bills (T-bills) mature in one year or less

- Treasury notes mature in 2 to 10 years

- Treasury bonds mature in 20 to 30 years

- TIPS (Treasury Inflation-Protected Securities) adjust their principal value based on inflation, providing protection against rising prices

In early 2024, 10-year Treasury yields hover around 4-4.5%, significantly higher than the near-zero rates of the 2010s. This has made Treasuries more attractive to income-focused investors, though yields fluctuate constantly based on Federal Reserve policy and economic conditions.

Corporate Bonds are issued by companies to raise capital for expansion, acquisitions, or day-to-day operations. These are riskier than Treasuries because companies can—and sometimes do—go bankrupt. To compensate for this extra risk, corporate bonds typically offer higher yields.

Corporate bonds are rated by agencies like Moody’s, Standard & Poor’s, and Fitch. Investment-grade bonds have ratings of BBB- or higher and are considered relatively safe. High-yield bonds (also called “junk bonds”) have lower ratings and offer higher yields to compensate for greater default risk. As a beginner, understanding this distinction matters—a AAA-rated corporate bond from a financially strong company is very different from a B-rated speculative issuance.

Municipal Bonds (Munis) are issued by state and local governments, as well as agencies like airport authorities or housing development corporations. They come in two main varieties: general obligation bonds, backed by the full taxing power of the issuer, and revenue bonds, backed by the revenue from specific projects (like toll roads or utility systems).

The big advantage of municipal bonds is that the interest they pay is often exempt from federal income tax and sometimes state and local taxes as well. For investors in high tax brackets, this tax advantage can make munis surprisingly attractive even when their pre-tax yields are lower than corporate bonds.

Agency Bonds are issued by government-sponsored enterprises like Fannie Mae (the Federal National Mortgage Association) or Freddie Mac (the Federal Home Loan Mortgage Corporation). These aren’t technically government-backed, but they’re widely considered to have implicit government support, making them nearly as safe as Treasuries while often offering slightly higher yields.

International Bonds issued by foreign governments or corporations add another layer of complexity. Currency fluctuations can amplify or reduce returns, and political risk varies by country. Most beginner investors can ignore this category entirely—there are plenty of domestic options to fill the bond allocation in a simple portfolio.

Should Beginners Invest in Bonds? The Pros and Cons

Here’s where I need to be honest with you: bonds aren’t always the right answer, and many financial articles oversell them to beginners. Let me walk through both sides.

The Case For Bonds

Lower volatility than stocks. This is bonds’ primary selling point. While the S&P 500 can drop 20% or more in a bad year, high-quality bonds typically move much less dramatically. During the 2008 financial crisis, while stocks plummeted, Treasury bonds actually rallied as investors fled to safety. This stability can help you sleep at night and prevent panic selling during market turbulence.

Predictable income stream. If you hold individual bonds to maturity, you know exactly what you’ll receive and when. Unlike dividends, which companies can cut or eliminate, bond coupon payments are contractual obligations. For retirees or anyone needing reliable cash flow, this predictability has genuine value.

Diversification benefits. Bonds often move inversely to stocks—when stocks fall, bonds tend to rise (though this relationship isn’t perfect). Adding bonds to a stock-heavy portfolio can reduce overall portfolio volatility without necessarily sacrificing all returns.

Capital preservation. If you’re saving for a goal within 3-10 years—buying a house, funding a wedding, paying for college—putting that money in stocks is risky. A market downturn right before you need the cash could devastate your plans. Bonds, especially short-term ones, offer a safer place to park money you’ll need soon.

Current yields are decent. After years of near-zero interest rates, bonds finally offer meaningful yields again. The 10-year Treasury yield above 4% is historically reasonable, and some corporate and municipal bonds are paying 5-6%. You can construct a bond portfolio generating 4-5% with relatively low risk, which is a far cry from the 1-2% yields of the early 2020s.

The Case Against Bonds (For Some Investors)

Lower long-term returns than stocks. Over very long periods, stocks have historically outperformed bonds by a significant margin. From 1928 through 2023, the S&P 500 returned roughly 10% annually on average, while long-term government bonds returned about 5%. Over 30 years, that difference compounds into hundreds of thousands of dollars on a $100,000 investment. If you’re young with a long time horizon, bonds may drag down your final portfolio value.

Interest rate risk is real and painful. When interest rates rise, bond prices fall—and the longer the bond’s maturity, the harder it gets hit. The 2022 bond market was a disaster: the Bloomberg U.S. Aggregate Bond Index, a broad measure of the U.S. bond market, lost over 13% in a single year. That’s the worst annual return in the index’s history. If you panic and sell during a rate-hike cycle, you can lock in losses.

Inflation can erode purchasing power. Fixed coupon payments lose value when inflation rises. If you’re earning 4% on your bonds but inflation runs at 5%, your real return is negative. TIPS offer some protection, but they add complexity and don’t always keep pace.

Complexity and selection challenges. Unlike buying an index fund for stocks, building a bond portfolio requires more decisions. Do you buy individual bonds or bond funds? Which maturities? What credit quality? These aren’t trivial questions, and the wrong choices can cost you.

Liquidity concerns. Some bonds, especially municipal bonds and certain corporate issuances, trade infrequently. You might not be able to sell quickly at a fair price if you need cash urgently.

The honest answer: whether bonds are right for you depends on your age, risk tolerance, time horizon, and financial goals. A 25-year-old saving for retirement probably doesn’t need much bond exposure. A 60-year-old five years from quitting work probably does.

How to Invest in Bonds as a Beginner

You have several pathways to invest in bonds, each with tradeoffs:

Direct purchase through a broker. Most online brokers—Fidelity, Charles Schwab, Vanguard, E*TRADE, TD Ameritrade—allow you to buy individual bonds at auction or in the secondary market. You’ll need to navigate the bond screeners, understand minimum purchases (often $1,000 or $10,000 for new issuances), and pay attention to transaction costs, which can be higher for bonds than for stocks.

Bond mutual funds. These pools of dozens or hundreds of bonds let you achieve diversification with a single purchase. You can buy shares in actively managed funds (where a manager selects the bonds) or index funds (which track a bond index). Expense ratios matter—Vanguard’s bond index funds charge as low as 0.03%, while actively managed funds might charge 0.6% or more.

Exchange-traded funds (ETFs). Bond ETFs trade like stocks throughout the day, offering liquidity that mutual funds don’t. Popular options include iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), Vanguard Total Bond Market ETF (BND), and iShares iBoxx $ High Yield Corporate Bond ETF (HYG). These are excellent choices for beginners because they provide instant diversification with low minimum investments (the price of one share).

Treasury Direct. The U.S. Treasury’s website lets you purchase Treasury bonds, notes, bills, and TIPS directly from the government, cutting out the middleman. This is a good option if you want to hold individual Treasuries and avoid broker markups. The website is clunky and the process can be slow, but the pricing is transparent.

For most beginners, a bond ETF is the simplest path. It gives you diversified bond exposure without the complexity of selecting individual bonds or paying high mutual fund fees. BND (Vanguard Total Bond Market ETF) gives you exposure to the entire U.S. investment-grade bond market in one holding. If you want to be more targeted, a mix of a short-term bond ETF, an intermediate-term Treasury ETF, and a corporate bond ETF can give you a basic ladder.

The minimum investment for most bond ETFs is simply the share price—often under $100. This is far more accessible than the $1,000+ minimums for individual bonds.

Common Bond Investment Risks

Every bond investor should understand these key risks:

Credit Risk is the possibility that the bond issuer defaults—fails to make interest payments or doesn’t repay the principal. Government bonds (especially U.S. Treasuries) have extremely low credit risk. Corporate bonds vary widely. You can assess credit risk by checking the bond’s rating from Moody’s, S&P, or Fitch. Investment-grade bonds (BBB- or higher) are safer; high-yield bonds carry meaningful default risk. In 2023, the default rate for high-yield corporate bonds was around 3-4%, meaning roughly 1 in 25 issuers failed to meet their obligations.

Interest Rate Risk is the risk that rising rates cause bond prices to fall. This is counterintuitive: when you hold a bond paying 3% and new bonds are paying 5%, your bond is less valuable. The longer the time until maturity, the more price sensitive the bond is to interest rate changes. Duration is the metric that measures this—higher duration means more risk.

Inflation Risk eats away at your fixed coupon payments. If inflation averages 4% annually and your bond pays 3%, you’re losing purchasing power over time. TIPS and short-term bonds offer some protection, but no bond is completely inflation-proof.

Liquidity Risk means you might not be able to sell your bond quickly at a fair price. Corporate bonds and municipal bonds can be illiquid, especially in stressed market conditions. During the COVID-19 market crash in March 2020, some bond funds suspended redemptions temporarily because they couldn’t sell holdings fast enough.

Call Risk applies to bonds that can be “called” (redeemed early) by the issuer. If interest rates fall, companies often call their higher-yielding bonds and reissue at lower rates, leaving you with your principal back but no place to reinvest at similar yields. Always check whether a bond is “callable” before buying.

Bonds vs Stocks: What’s Better for Beginners?

This is the wrong question. Both have a place in a sensible portfolio; the answer depends entirely on your situation.

If you’re under 30 and investing for retirement 30+ years away, you can afford to take risk. Most of your portfolio should probably be in stocks because they offer superior long-term growth. A common rule of thumb—subtract your age from 110 to get your stock allocation—isn’t bad. At 25, you’d hold 85% stocks, 15% bonds. At 50, you’d be closer to 60/40.

If you’re 60 and retiring in five years, the calculation changes dramatically. You need that money soon and can’t afford a 40% stock market decline right before you start withdrawing. More conservative allocations—40% stocks, 60% bonds, or even more bond-heavy—make sense.

But here’s what many articles don’t tell you: the traditional “age in bonds” rule has been questioned by modern financial research. During periods of low returns (like the 2010s), holding too much in bonds could leave you with insufficient retirement savings. Some experts now suggest younger investors keep 90%+ in stocks, accepting short-term volatility for better long-term growth.

The key insight is that bonds and stocks serve different purposes. Stocks are for growth. Bonds are for stability, income, and capital preservation. Neither is inherently “better”—they’re tools for different jobs. A portfolio with only stocks has no shock absorber for downturns. A portfolio with only bonds may not generate enough growth to meet long-term goals. Most investors benefit from both.

Frequently Asked Questions

How much money do I need to start investing in bonds?

For bond ETFs, you can start with the price of one share—often under $100. For individual bonds, expect minimums of $1,000 to $10,000. Bond mutual funds typically have minimums of $3,000 or less. Treasury Direct allows purchases starting at $100.

Are bonds safer than stocks?

Generally, yes—high-quality bonds are less volatile and rank higher in the payment priority if an issuer goes bankrupt. However, “safer” doesn’t mean “risk-free.” Bond prices can fall significantly during interest rate hikes, and some bonds (junk bonds) carry substantial default risk. In a diversified portfolio, bonds typically serve as the less volatile counterweight to stocks.

What happens to bonds when interest rates fall?

When rates fall, existing bonds with higher coupon rates become more valuable, and their prices rise. If you hold a bond to maturity, you don’t care about price fluctuations—you’ll receive your fixed coupon payments and get your principal back at maturity. However, when rates fall, your bond’s yield to maturity also declines, meaning reinvested coupon payments will earn less.

Can you lose money on bonds?

Yes. If you sell a bond before maturity and interest rates have risen, you’ll sell at a loss. If the issuer defaults, you could lose some or all of your principal. During 2022, the broad U.S. bond market had its worst year in history, losing over 13%. These losses are normal and expected in certain environments.

Should I buy bonds through a 401(k) or IRA?

Yes—if you have a 401(k) or IRA, holding bonds inside these tax-advantaged accounts is usually smart because bond income is taxed as ordinary income, which is the least tax-efficient type of income. Putting bonds in tax-advantaged accounts and stocks in taxable accounts is a common optimization strategy.

Conclusion: The Honest Answer

Bonds are not exciting. They won’t make you rich quickly. They’re the financial equivalent of eating vegetables—nobody raves about broccoli, but it’s good for you.

If you’re young with decades until retirement, you probably don’t need many bonds right now. The growth potential of stocks outweighs the stability benefits of bonds. But as you approach your goals—whether that’s buying a home, funding education, or retiring—bonds should start occupying a larger share of your portfolio.

The practical move: open a brokerage account if you don’t have one, look at a low-cost bond ETF like BND, and start small. You don’t need to figure out your entire bond strategy today. But you should understand what they are and why they matter, because at some point in your financial life, they will.

Whether that point is next year or 30 years from now depends on your goals. But the foundation of knowledge is the same either way.