The Rule of 72 is a financial concept that provides a quick mental shortcut for estimating how long it takes for an investment to double in value, based on a fixed rate of return. Instead of pulling out a calculator or building a compound interest spreadsheet, investors can use this formula to make reasonably accurate projections in seconds. The formula is straightforward: divide 72 by your expected annual return, and the result tells you approximately how many years until your money grows to twice its original amount.

This makes the Rule of 72 particularly useful when comparing investment options or setting expectations for retirement planning. Many people overestimate how quickly their money grows, and this simple formula provides a reality check. Below, I’ll walk through the formula itself, work through examples, explain why it works mathematically, and explore the limitations that every investor should understand.

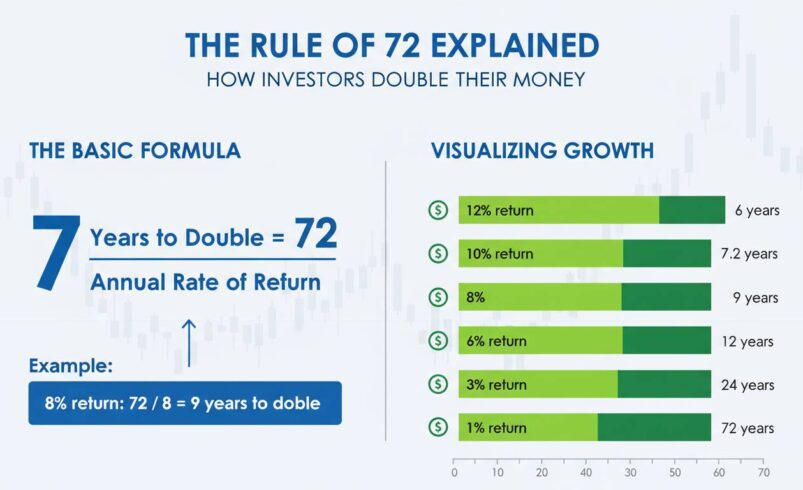

The Rule of 72 Formula

The formula is:

Years to Double = 72 ÷ Interest Rate

The number 72 serves as the numerator, and you divide it by your expected annual interest rate expressed as a whole number rather than a decimal. If you anticipate an 8% annual return, divide 72 by 8, giving you 9 years to double your money. At a 6% return, divide 72 by 6 to get 12 years. At 12%, divide 72 by 12 to arrive at 6 years.

The formula assumes compound interest, where returns are reinvested rather than withdrawn, which is the standard approach for long-term investment accounts like 401(k)s and IRAs. It also assumes a fixed annual rate of return, which is important to note because actual market returns fluctuate year to year.

The formula works well within a practical range of interest rates. Between rates of 2% and 10%, the Rule of 72 produces estimates that are close to actual compound interest calculations, typically within a year or less of the precise figure. This accuracy, combined with the ease of mental calculation, explains why the formula has persisted for centuries.

How to Calculate Using the Rule of 72

Here are several practical examples.

Example 1: The Conservative Investor

Consider a conservative investor who puts $10,000 into a diversified portfolio expecting a 4% annual return. Using the Rule of 72, divide 72 by 4, which gives 18 years. At the end of 18 years, that $10,000 would grow to approximately $20,000. For comparison, the actual compound interest calculation using the formula for doubling time (years = ln(2) / ln(1 + r)) yields 17.67 years—a difference of only about 4 months.

Example 2: The Moderate Investor

A moderate investor with a 60/40 stock/bond allocation might expect a 7% average annual return over the long term. Dividing 72 by 7 gives approximately 10.3 years to double money. If this investor started with $50,000 at age 35, they would have roughly $100,000 by age 45 or 46. The actual precise calculation yields 10.24 years, meaning the Rule of 72 is off by less than a month.

Example 3: The Aggressive Investor

An aggressive investor targeting a 10% return—which approximates the historical average return of the S&P 500 over very long periods—would divide 72 by 10 to find that their money doubles approximately every 7.2 years. Starting with $25,000, this investor would reach $50,000 in about 7 years, $100,000 in about 14 years, and $200,000 in about 21 years. The actual precise calculation gives 7.27 years, so the Rule of 72 is off by only a few weeks.

Example 4: Very Low Rates

The formula loses accuracy at extremely low interest rates. At a 2% return, the Rule of 72 predicts 36 years to double (72 ÷ 2), but the actual precise calculation is 34.87 years—a difference of more than a year. This overestimation occurs because the mathematical constant that approximates compound growth (69.3, when using natural logarithms) is lower than 72, and this gap widens at lower rates.

Why the Rule of 72 Works

The mathematical foundation behind the Rule of 72 involves the nature of compound interest and natural logarithms. The precise formula for determining doubling time is: Years = ln(2) / ln(1 + r), where ln represents the natural logarithm and r represents the interest rate as a decimal.

The natural logarithm of 2 equals approximately 0.693. For small interest rates, ln(1 + r) is approximately equal to r itself. This means that for reasonable interest rates, the doubling time is roughly 0.693 divided by r. When r is expressed as a percentage rather than a decimal, this becomes 69.3 ÷ rate.

So why use 72 instead of 69.3? Several reasons make 72 more practical in everyday use. First, 72 is divisible by more whole numbers than 69 or 70, making mental calculations easier. It divides evenly by 2, 3, 4, 6, 8, 9, 12, 18, 24, and 36, whereas 69 and 70 have more limited divisibility. Second, 72 produces slightly higher (more conservative) estimates than the mathematically precise 69.3, which can be useful when setting expectations. Third, for interest rates in the common range of 6% to 10%, the number 72 produces results that are closer to actual doubling times than 69.3 would provide.

The choice of 72 is a pragmatic compromise between mathematical precision and computational convenience.

Limitations of the Rule of 72

The Rule of 72 is a useful approximation, but it has limitations that sophisticated investors must understand.

At extreme interest rates, accuracy suffers significantly. At a 1% interest rate, the formula predicts 72 years to double, while the actual time is 69.66 years—a 2.3-year error. At 1%, this might not seem catastrophic, but consider that many savings accounts and bonds currently offer rates in this range, and the prediction becomes misleading. At 20%—which might apply to certain high-yield investments or margin accounts—the formula predicts 3.6 years while actual doubling occurs in 3.8 years. The formula actually becomes more accurate at moderate rates between 4% and 12%, which happens to be the range most relevant to long-term equity investors.

The formula assumes a fixed rate of return. In reality, investment returns vary significantly year to year. The S&P 500 might return 30% one year and lose 20% the next. The Rule of 72 provides an answer based on a constant return, which rarely matches reality. A portfolio that averages 8% might actually take longer to double if it experiences significant losses early in the holding period, because there’s less principal available to compound during the recovery years.

Inflation is not factored into the calculation. The Rule of 72 calculates nominal doubling time—the number of years until your account balance doubles. It doesn’t account for inflation eroding purchasing power. If inflation averages 3% annually and your investment returns 6%, your real return is only 3%, meaning it would take 24 nominal years to double your money, but the purchasing power would only have doubled at the 24-year mark.

The Rule of 72 says nothing about risk. Higher expected returns almost always come with higher risk. A strategy targeting 12% returns might involve concentrated positions in volatile sectors, while a 4% return might come from Treasury bonds. The formula provides no guidance on whether a given rate of return is achievable or advisable for your specific risk tolerance and time horizon.

For these reasons, the Rule of 72 works best as a quick estimation tool, not as a basis for retirement calculations or major financial decisions. When precision matters, use a proper compound interest calculator that accounts for your specific situation.

How Investors Use the Rule of 72

Despite its limitations, the Rule of 72 serves several practical purposes in investment planning and decision-making.

Setting realistic time horizons. One of the most valuable applications is calibrating expectations about when invested money will grow substantially. I once discussed retirement with a client who expected to double his money three times in 20 years, which would require an average annual return of over 20%—a return level that would place his portfolio in the top 0.1% of all professionally managed funds. When I showed him using the Rule of 72 that a more realistic 7% return would take 10 years per doubling, his entire retirement timeline shifted. He needed to save significantly more or retire later than he had planned.

Comparing investment options. When evaluating different investment choices, the Rule of 72 provides a quick framework for comparison. If one investment offers a 5% guaranteed return and another offers 8% with some risk, you can instantly see that the riskier option might double your money in 9 years versus 14 years for the safer option. This doesn’t make the riskier option correct—it simply provides context for whether the additional risk/reward tradeoff makes sense for your goals.

Understanding the impact of fees. Investment fees have a significant effect on long-term returns that many people underestimate. Consider two funds: one charges 0.5% annually while the other charges 1.5%. At an 8% gross return, the lower-cost fund nets 7.5%, doubling money in approximately 9.6 years. The higher-cost fund nets 6.5%, doubling in approximately 11.1 years. Over a 30-year period, this 1% fee difference can reduce your final portfolio value by 25% or more.

Teaching financial literacy. The Rule of 72 is simple enough that children can understand it, yet it demonstrates one of the most powerful concepts in finance: compound interest. Teaching young people about compound interest using this formula can change how they think about saving and investing.

Related Rules: The Rule of 70 and Rule of 115

While the Rule of 72 is the most commonly used, related formulas serve different purposes.

The Rule of 70 works identically to the Rule of 72 but uses 70 as the numerator. Some financial educators prefer it because it’s mathematically closer to the precise constant (69.3) and therefore slightly more accurate at very low interest rates. At a 3% return, the Rule of 70 predicts 23.3 years versus the Rule of 72 prediction of 24 years, with the actual being 23.1 years. For conservative investors focusing on lower returns, the Rule of 70 provides a marginally more accurate estimate.

The Rule of 115 extends the concept to tripling money rather than doubling it. Divide 115 by your interest rate to estimate years until your investment triples. At an 8% return, 115 ÷ 8 = 14.4 years to triple. This is useful for investors who want to think beyond simple doubling to larger potential growth scenarios.

Common Questions About the Rule of 72

Can the Rule of 72 be used for debt? Yes. The same math that makes compound interest your friend when investing makes it your enemy when borrowing. Credit card debt at 24% annual interest, for example, will approximately double the amount you owe in just 3 years (72 ÷ 24 = 3). This is why paying down high-interest debt should typically take priority over investing.

Who invented the Rule of 72? The concept is often attributed to Luca Pacioli, a 15th-century Italian mathematician who wrote about it in his 1494 book “Summa de Arithmetica.” However, the underlying mathematical relationship was likely understood by earlier scholars, and some historians credit the formula to earlier Arabic or Hindu mathematicians. Pacioli gets credit primarily because his book was widely printed and preserved, making the method accessible to later European mathematicians and accountants.

How accurate is the Rule of 72 really? Within the 4% to 12% interest rate range—which covers most investment scenarios—the Rule of 72 is accurate to within about 6 months of the actual doubling time. Outside this range, accuracy decreases. At 2%, it overestimates by about 1.3 years. At 15%, it underestimates by about 0.4 years.

Does the Rule of 72 work for monthly returns? The formula applies to annual returns. For monthly returns, you would need to annualize the monthly rate first (multiply by 12), then apply the Rule of 72.

Conclusion

The Rule of 72 endures because it solves a genuine problem: investors need quick ways to estimate growth without complex calculations, and this formula delivers reasonable accuracy with minimal effort. It’s not a replacement for detailed financial planning, but it’s a helpful mental model that helps investors set realistic expectations and make informed comparisons.

What strikes me after years of working with clients on financial planning is how often the Rule of 72 serves as a reality check. People arrive with optimistic assumptions about how quickly their money will grow, and a quick division problem often reveals that their timeline expectations were off base. That moment of recalibration—seeing that “quick doubling” actually takes a decade or more at reasonable return rates—is worth more than any spreadsheet.

This caveat is worth remembering: the formula works best as a starting point for thinking about time and returns, not as a precision tool. Markets don’t deliver constant returns, inflation eats into real gains, and fees compound against you just as surely as interest compounds for you. Use the Rule of 72 to frame the conversation, then dive deeper with tools that account for your actual circumstances.