The biggest lie in value investing is that a low price makes a stock cheap. I’ve watched investors pile into seemingly battered companies only to watch their portfolios bleed out for years, convinced they were being “patient” when they were actually holding a value trap. The difference between picking genuine bargains and catching a falling knife comes down to understanding what you’re actually buying — and more importantly, why the market has priced it so low.

This guide gives you a practical framework to distinguish between a legitimate value opportunity and a stock that deserves its discount. I’ll walk through the financial metrics that matter, the warning signs most investors miss, and the mindset shifts that will save you from the most costly mistakes in value investing.

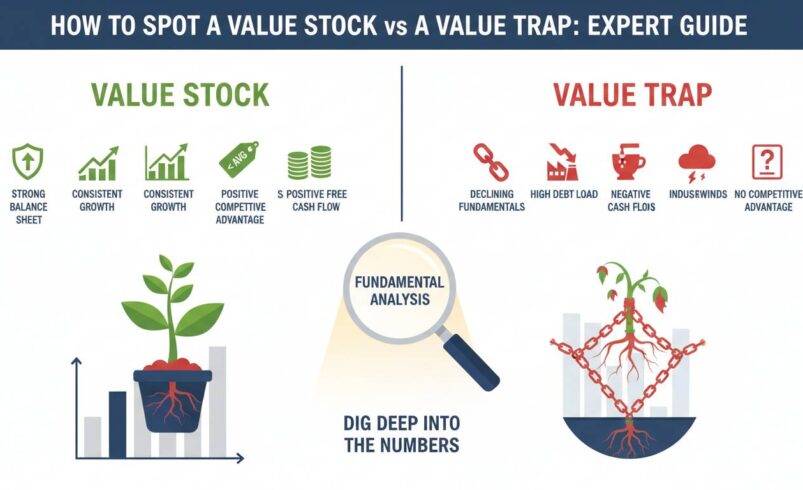

What Actually Defines a Value Stock

A value stock is a company trading below what its fundamentals — earnings, assets, cash flow — would suggest it’s worth. The premise is simple: the market has overreacted to short-term problems, creating an opportunity to buy quality at a discount.

What separates a true value stock from a mirage is whether the business itself is sound. You’re not just buying a low multiple; you’re buying a company with sustainable economics, manageable debt, and a path to realizing its intrinsic value. True value stocks often trade at low P/E ratios because the market has temporarily lost faith in the company’s ability to generate future earnings. But that faith is misplaced — the company’s competitive position remains intact, and the fundamentals will recover.

Consider this: when Amazon’s stock plummeted during the dot-com crash, it was technically expensive by traditional metrics. But companies like Johnson & Johnson or Procter & Gamble have periodically traded at low multiples during market corrections precisely because investors overreacted to temporary headwinds. These are the moments when genuine value stocks emerge.

The key characteristic of a true value stock is that it has an “edge” — something about its business that will allow it to generate returns above what the current price implies. Maybe it’s brand strength, a dominant market position, pricing power, or operational efficiencies competitors can’t replicate. Without that edge, you’re not investing in a value stock; you’re gambling that someone will bail you out at a higher price.

What Makes a Stock a Value Trap

A value trap is a stock that looks cheap by traditional metrics but continues declining — or never recovers — because the underlying business is deteriorating. The “trap” part comes from the seductive appeal of the low price. It feels like a bargain, so investors convince themselves to hold, hoping for a turnaround that never materializes.

The critical distinction is that value traps often look attractive precisely because the market is correctly pricing in future decline. Those low P/E ratios aren’t a sign of undervaluation; they’re a reflection of shrinking earnings. The dividend yield might look appealing, but it’s being paid from dwindling cash flows or, worse, debt.

Think about retail stocks that traded at single-digit P/E ratios throughout the 2010s. Companies like Sears, JCPenney, and Bed Bath & Beyond all looked “cheap” on paper. The market wasn’t wrong about their trajectories — it was right. The low multiples reflected a business model being destroyed by e-commerce competition. Investors who bought these “value” stocks lost massive amounts of capital.

A value trap often exhibits one or more of these characteristics: declining market share, technological obsolescence, unsustainable debt levels, or an industry in structural decline. The market pricing reflects reality; the trap is thinking the price is wrong when it’s actually right.

Key Financial Metrics That Reveal the Truth

Most investors rely too heavily on a single ratio — the P/E multiple — and miss the story the full financial picture tells. Here’s what actually matters when evaluating whether a stock is a value or a trap.

Price-to-Earnings Ratio (P/E): A low P/E is the starting point, not the answer. Divide the stock price by earnings per share, but always ask what earnings are being measured. Trailing P/E uses past earnings; forward P/E uses estimated future earnings. If a stock trades at 8x trailing earnings but 15x forward earnings, the “cheap” multiple is an illusion.

Price-to-Book Ratio (P/B): This matters most for asset-heavy businesses — banks, insurers, real estate, industrial companies. A P/B below 1 sometimes signals undervaluation, but it can also mean the market believes the assets on the balance sheet are overvalued or impaired. Always review the actual asset quality, not just the ratio.

Debt-to-Equity Ratio: This is where many value traps reveal themselves. Companies with high debt levels face interest payments that consume cash flow during downturns. A telecommunications company or utility with moderate debt is manageable; a retailer or manufacturer with debt exceeding equity is a warning sign. Calculate net debt (total debt minus cash) to get the real picture.

Free Cash Flow: Earnings can be manipulated through accounting choices. Free cash flow — what remains after capital expenditures — cannot. A company generating robust free cash flow has optionality: it can return capital to shareholders, invest in growth, or weather downturns. A company burning cash is living on borrowed time.

Return on Equity (ROE): This measures how efficiently a company uses shareholder capital. A consistently high ROE suggests a durable competitive advantage. A declining ROE signals erosion of that advantage — exactly what you find in value traps.

The key is looking at these metrics across multiple years, not a single snapshot. A value stock shows consistent (or improving) fundamentals despite temporary setbacks. A value trap shows deterioration that the low multiple obscures.

Five Red Flags That Signal a Value Trap

I’ve developed a mental checklist from years of analyzing turnaround situations. If you spot these warning signs, the “cheap” price is probably warranted.

Declining revenue with no credible turnaround plan: A stock can survive one or two bad years if management has a clear strategy to recover. But if revenue has been shrinking for multiple years and the CEO’s answer to “how do you fix this” involves vague talk about “operational efficiency” or “exploring strategic alternatives,” you’re looking at a business in structural decline.

Management with a track record of value destruction: Look at the CEO’s history. Have they consistently made decisions that benefit shareholders? Or do they have a pattern of issuing shares at lows, approving acquisitions that destroy value, or receiving generous compensation while the stock languishes? Words are cheap; actions reveal character.

Competitive position deteriorating: This is the most important factor, and it’s qualitative, not quantitative. Ask yourself: is this company gaining or losing market share? Are customers choosing this product over alternatives? Is the product or service becoming obsolete? You can find this information in 10-K filings, earnings call transcripts, and industry reports. If competitors are eating this company’s lunch, the low price reflects reality.

Dividends that aren’t sustainable: A high dividend yield looks attractive, but it’s only valuable if the company can maintain it. Look at the payout ratio (dividends divided by earnings or free cash flow). A ratio above 80-90% means the dividend is at risk. Also check whether the dividend was raised during good years and cut during bad ones — consistency matters more than yield.

Insider selling or institutional abandonment: When management and large shareholders are selling, pay attention. While there are legitimate reasons for selling (diversification, estate planning), sustained selling by insiders is a powerful signal that those closest to the company believe the stock is fairly valued or worse. Similarly, watch for declining institutional ownership — smart money often exits before retail investors realize there’s a problem.

Positive Indicators of a Genuine Value Stock

Now for the other side of the coin. These signals suggest you’ve found a legitimate opportunity rather than a trap.

Strong free cash flow generation: This is the ultimate test. A company producing more cash than it needs to operate and grow is fundamentally healthy, regardless of what the P/E ratio says. Look for companies generating free cash flow consistently, especially if that cash flow is growing over time. This provides a margin of safety — even if the business faces headwinds, the cash cushion provides options.

Durable competitive advantages: The best value stocks have what Warren Buffett calls “moats” — something that protects them from competitors. This could be a powerful brand (Apple, Coca-Cola), a network effect (Visa, Mastercard), regulatory barriers (utilities, insurers), or economies of scale (Walmart, Amazon). The moat doesn’t have to be permanent, but it needs to be sustainable for the foreseeable future.

Management with skin in the game: Look for management teams that own significant stock and have a track record of smart capital allocation. The best CEOs think like owners — they return capital when returns are low, invest aggressively when returns are high, and avoid the ego-driven empire building that destroys shareholder value. Compensation structures that align management with shareholders are a positive sign.

A clear catalyst for revaluation: True value stocks often have a specific event or timeline that will cause the market to recognize their worth. This could be a management change, a spin-off, a share repurchase program, an activist investor intervention, or simply the market recognizing that temporary problems have passed. Without a catalyst, you might be right about the value but wrong about the timing — and timing matters for your portfolio.

Capital return programs: Companies that consistently repurchase shares at reasonable valuations and pay growing dividends demonstrate a commitment to shareholder returns. This is particularly meaningful when the stock trades below intrinsic value — buybacks at a discount create per-share value for remaining shareholders. Look for companies with long track records of returning capital, not just opportunistic repurchases during stock slumps.

How to Research a Stock Before Buying

Understanding the theory is one thing; applying it is another. Here’s a practical research process to work through before committing capital.

Start with the 10-K filing — the annual report required by the SEC. Read the business description to understand what the company does, how it makes money, and what risks it faces. Then review the financial statements: balance sheet, income statement, and cash flow statement. Look for trends over five years, not just the most recent quarter.

Calculate the key metrics yourself rather than relying on screeners. A company might report “adjusted” earnings that exclude one-time charges — dig into the footnotes to see what’s being adjusted. The notes often reveal problems management would prefer you miss.

Next, read the most recent quarterly earnings call transcript. Listen for what management says about the competitive environment, pricing power, and capital allocation plans. Pay attention to what they don’t discuss as much as what they do. Analysts’ questions often reveal concerns that aren’t apparent in the press release.

Finally, understand the story the market is telling. Why is this stock cheap? Is it a temporary problem (which might create a value opportunity) or a structural one (which likely signals a value trap)? The answer determines whether you’re a potential buyer or should look elsewhere.

Common Mistakes That Cost Investors Dearly

After years of analyzing investments and watching others make decisions, I’ve seen the same errors repeat themselves. Avoiding these will dramatically improve your results.

Chasing yield: High-yielding stocks attract investors seeking income, but yield alone tells you nothing about sustainability. During the 2008 financial crisis, banks like Bank of America and Citigroup cut their dividends to near-zero because the payouts were unsustainable. Investors who bought for yield were devastated. Always evaluate the dividend in context of the company’s ability to maintain it through full economic cycles.

Ignoring the balance sheet: Earnings can be manipulated; balance sheets don’t lie as easily. A company with too much debt has less flexibility to survive downturns. During the pandemic, companies with strong balance sheets (think Microsoft, Apple) could weather the storm, while heavily indebted competitors faced bankruptcy. The balance sheet is your margin of safety.

Falling in love with the story: Investors sometimes become convinced a company will turn around despite mounting evidence to the contrary. Confirmation bias leads them to seek out bullish opinions while ignoring bearish ones. The solution is simple but hard: be willing to accept when you’re wrong. Set predetermined sell criteria before you buy, and stick to them.

Timing the bottom: Trying to catch a falling knife is a loser’s game. Even great value stocks can decline further after you buy them. Rather than trying to time the bottom, buy in stages — establish a position, and add to it if the price drops further. This removes the psychological pressure of being “right” on entry.

Conclusion

The distinction between a value stock and a value trap comes down to one question: is the business getting stronger or weaker? Low multiples are meaningless if the earnings themselves are declining. The market is generally efficient at pricing in known information — the opportunity in value investing comes from finding situations where the market has overreacted to short-term problems and assumed they’re permanent.

True value investing requires intellectual honesty. It means being willing to say “I was wrong” when the fundamentals deteriorate, rather than doubling down on a losing position because the price feels “cheap.” It means doing the hard work of understanding a business deeply before committing capital, rather than relying on screeners and hot tips.

The investors who succeed in value investing are those who maintain a skeptical mindset, do their own research, and prioritize capital preservation over the seduction of “bargain” prices. The market will give you plenty of opportunities to prove you’re smarter than the consensus — but most of those opportunities are traps.