The market is plummeting. Your portfolio is bleeding. Then, without warning, trading stops. For fifteen minutes—or potentially the rest of the day—you watch the screen freeze while the exchange tries to figure out what just happened. That’s a circuit breaker in action. If you’ve been investing for any meaningful time, you’ve probably experienced that mix of market panic and forced stillness.

This guide covers what stock market circuit breakers are, how they function at each trigger level, the differences between NYSE and derivatives market rules, and why these safeguards remain one of the most debated tools in market infrastructure. Whether you’re a new investor trying to decode the evening news or a seasoned trader wanting to understand the mechanics behind those unexpected trading halts, by the end of this piece you’ll have a working knowledge that goes well beyond the superficial explanations you’ll find in most financial media.

What Are Circuit Breakers?

Circuit breakers are automated trading halts designed to prevent panic-selling from spiraling into a complete market collapse. When the Dow Jones Industrial Average drops by a predetermined percentage from the previous day’s closing price, exchanges trigger a temporary pause in trading. This gives participants time to absorb new information, reassess their positions, and—ideally—make more rational decisions rather than reactions driven by fear.

The system operates on a tiered basis. The first circuit breaker triggers at a 7% decline, the second at 13%, and the final tier activates at 20%. Each successive level brings longer halt durations, with the most severe drops potentially shutting down markets for the remainder of the trading day.

These mechanisms exist because markets, despite their reputation for rationality, are susceptible to cascading failures. A large sell order can trigger algorithmic responses, which beget more selling, which triggers more algorithms—a feedback loop that can decimate valuations in minutes. The 1987 Black Monday crash demonstrated this vulnerability: the Dow Jones Industrial Average fell 22.6% in a single trading session, a decline that occurred in roughly three hours. No circuit breakers existed then. Regulators decided never to let that happen again without some kind of guardrail.

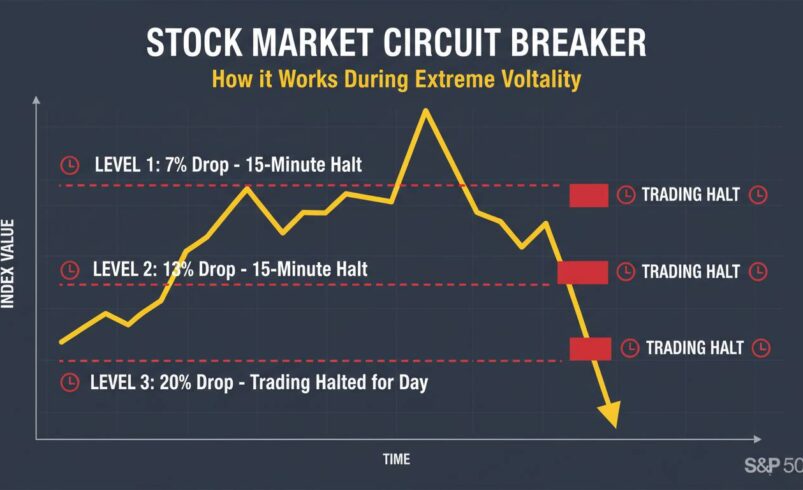

The Three Circuit Breaker Levels

Level 1: The 7% Decline

When the S&P 500 falls 7% from the previous day’s closing price before 3:25 PM ET, trading halts for 15 minutes. This is the most commonly triggered level, designed to address moderate but concerning market stress. The halt gives market participants a chance to catch their breath and evaluate whether the selling pressure reflects fundamental concerns or temporary panic.

If the decline occurs after 3:25 PM, the market does not halt. This rule exists because trading volumes thin significantly in the final minutes of the session, and a halt during those periods would accomplish little while potentially creating settlement complications.

Level 2: The 13% Decline

If selling pressure continues and the S&P 500 reaches a 13% decline from the prior close, another 15-minute halt triggers (assuming it’s before 3:25 PM). At this point, the market has experienced significant trauma, and regulators want additional time for information to disseminate and for buyers to potentially step in at distressed prices.

The 13% threshold has historically been less common than Level 1 triggers, largely because many market dislocations resolve themselves before reaching this severity. However, during periods of extreme stress—such as the early days of the COVID-19 pandemic in March 2020—Level 2 activations become realistic scenarios.

Level 3: The 20% Decline

A 20% decline represents catastrophic market stress. When this threshold hits, trading halts for the remainder of the day. Markets simply close. This has only happened once in the modern circuit breaker era: on October 27, 1997, during the Asian Financial Crisis panic, when the Hong Kong market’s collapse triggered a domino effect that briefly terrified global investors.

A Level 3 trigger is designed to be apocalyptic. The idea is that if markets are falling this dramatically, something fundamental has gone wrong—perhaps a geopolitical crisis, a terrorist attack, or a financial system collapse—and continued trading under those conditions serves no constructive purpose.

How Circuit Breakers Are Triggered

The trigger mechanism differs between the New York Stock Exchange and the derivatives exchanges run by CME Group (which includes the Chicago Board Options Exchange). Understanding this distinction matters because these markets are interconnected.

NYSE Equity Market Rules

On the NYSE, circuit breakers apply to trading in individual stocks as well as to the broader market. The exchange uses “Limit Up-Limit Down” bands for individual securities, which prevent trades from occurring outside a certain price band relative to the recent trading average. This is different from the market-wide circuit breakers that apply to the S&P 500 index.

When the S&P 500 declines trigger a circuit breaker, all trading on the NYSE floor halts. Electronic traders also must pause. Market makers pull their quotes. The entire ecosystem freezes.

CME and Derivatives Markets

The CME Group operates separately, with its own circuit breaker structure for futures and options on the S&P 500 (symbol: ES), as well as for crude oil, gold, and other commodities. CME’s rules are slightly different from the NYSE’s and operate on a “cooling-off period” model rather than a hard halt in some cases.

For equity index futures, CME uses a 5%, 10%, and 20% decline structure tied to the prior day’s settlement price. These often trigger before the NYSE equivalents because futures lead cash markets by seconds or minutes. When CME circuit breakers activate, it frequently signals that trouble is coming for the equity markets as well.

The intermarket nature of circuit breakers creates interesting dynamics. A sharp drop in Asian markets might trigger CME futures selling, which could cascade into a US market circuit breaker even before US economic news has been released. This is precisely the kind of cross-market panic that circuit breakers are designed to interrupt.

A Brief History of Circuit Breakers

1987: The Birth of Modern Circuit Breakers

On October 19, 1987, the Dow Jones Industrial Average crashed 22.6% in a single day—the largest one-day percentage decline in Wall Street history. The cause was a perfect storm: rising interest rates, overvaluation concerns, and the nascent spread of portfolio insurance, a derivatives strategy that automatically sold stock index futures as markets fell. The automated selling created a feedback loop that accelerated the crash beyond anyone’s predictions.

The Brady Commission, investigating the crash, recommended market-wide trading halts. By 1988, the NYSE had implemented circuit breakers, though initially with different trigger points than today. The original system used point drops rather than percentages—a legacy of an era when the Dow was measured in hundreds rather than tens of thousands.

1997: The Asian Financial Crisis Test

The first (and still only) actual deployment of a Level 3 circuit breaker occurred on October 27, 1997, when the Dow fell 554 points (7.2%) before recovering. Wait—technically, that was a Level 1 trigger that happened to feel catastrophic. The 20% Level 3 threshold, however, was nearly triggered that same week as panic spread from Hong Kong’s market collapse.

In the aftermath, the SEC and exchanges revised the circuit breaker rules, lowering the thresholds from their original levels (which had been set too high to trigger during 1987’s crash) and standardizing on percentage-based triggers rather than point drops.

2013: The Flash Crash Rewrite

On May 6, 2010, a single large sell order in futures markets triggered what became known as the “Flash Crash.” The Dow lost nearly 1,000 points in minutes before recovering most of those losses by the close. The existing circuit breakers had failed to activate because the move was too fast.

This exposed a critical flaw: circuit breakers needed to respond to the speed of modern algorithmic trading. In 2013, the SEC and exchanges implemented new rules, including the Limit Up-Limit Down mechanism for individual stocks and revised circuit breaker thresholds designed to handle both slow-motion crashes and flash crashes. The current 7%/13%/20% structure dates from this 2013 overhaul.

Real Examples of Circuit Breakers in Action

March 16, 2020: COVID-19 Crash

During the COVID-19 market panic, the S&P 500 triggered a Level 1 circuit breaker on March 9, March 12, March 16, and March 18, 2020—six times in total across that brutal month. On March 16 specifically, the market opened down nearly 8% and hit the 7% threshold before 9:34 AM, triggering the first of four 15-minute halts that day.

What made this period remarkable was the frequency. Most investors had never experienced a circuit breaker trigger. Suddenly, they were experiencing them weekly. The market ultimately bottomed on March 23, 2020, and began one of the fastest recoveries in history—but the circuit breakers had done their job: they prevented the panic from becoming a total rout.

August 24, 2015: China Devaluation

When China unexpectedly devalued its currency in August 2015, global markets convulsed. The S&P 500 hit the 7% circuit breaker threshold before noon on August 24, 2015, marking the first circuit breaker trigger since the 2013 rule changes. Trading halted, headlines screamed, and then trading resumed. The market closed down 3.9%—significant, but not catastrophic.

October 15, 2014: The Mystery Flash Crash

On October 15, 2014, the Treasury yield and stock markets experienced wild swings without any obvious news catalyst. The Dow moved 400 points in minutes. The episode raised questions about whether high-frequency trading firms were manipulating markets—a debate that continues to this day. No circuit breakers were triggered because the moves, while dramatic, didn’t reach the percentage thresholds.

Do Circuit Breakers Actually Work?

Here’s where honest analysis requires some nuance. Circuit breakers accomplish their stated goal—preventing catastrophic, single-day crashes—but they introduce their own set of problems.

The case for circuit breakers: They provide breathing room during genuine crises. When markets are in freefall, a 15-minute pause can interrupt the panic spiral. Investors can reassess. Buyers might emerge at lower prices. The 2020 experience demonstrated that circuit breakers didn’t stop the market from eventually finding a bottom, but they may have prevented that bottom from being reached via a complete psychological collapse.

The criticism: Critics argue that circuit breakers create “moral hazard” for large traders. If you know the market will halt at a certain point, you can structure trades to trigger the halt and then exploit the disrupted pricing afterward. More fundamentally, some economists argue that letting markets find their own bottom—even a painful one—is preferable to artificial intervention that may delay necessary price discovery.

There’s also the problem of “tail risk.” Circuit breakers protect against catastrophic crashes but do nothing for “slow crashes” that unfold over weeks or months. The 2007-2009 financial crisis saw no circuit breaker triggers because the decline was gradual and sustained. Circuit breakers are designed for acute panic, not chronic deterioration.

Another issue that’s often overlooked: circuit breakers can concentrate trading at specific price points, creating artificial liquidity squeezes when trading resumes. The opening minutes after a halt often see heightened volatility as the market “discovers” the new equilibrium price.

Frequently Asked Questions

What are circuit breakers in the stock market?

Circuit breakers are automated mechanisms that temporarily halt trading when the market experiences significant declines. They operate on a tiered system—7%, 13%, and 20% drops from the prior day’s close—each triggering progressively longer pauses designed to curb panic selling and allow market participants to process new information rationally.

How do stock market circuit breakers work?

When the S&P 500 falls to one of the preset threshold percentages before 3:25 PM ET, the NYSE halts all trading for 15 minutes (or the remainder of the day for a 20% decline). During the halt, no buy or sell orders execute, and market makers withdraw quotes. Trading resumes only when the exchange determines conditions have stabilized. The CME Group operates similar but separate rules for futures and options markets.

When was the last time circuit breakers were triggered?

The most recent circuit breaker triggers occurred during the COVID-19 market crash in March 2020, when Level 1 (7%) circuit breakers were triggered on March 9, 12, 16, and 18. The last Level 2 (13%) trigger was on March 16, 2020. No Level 3 (20%) circuit breaker has been triggered since the modern system was implemented in 2013.

Do circuit breakers apply to individual stocks?

Yes, but through a different mechanism. Individual stocks on the NYSE and Nasdaq are subject to “Limit Up-Limit Down” rules, which halt trading for five minutes when a stock’s price moves beyond a specified band relative to its recent average price. This is designed to prevent extreme price swings in individual securities rather than the broader market.

Are circuit breakers the same worldwide?

No. The US system (7%/13%/20% on the S&P 500) is specific to American markets. Other exchanges have their own variations. Japan’s market circuit breaker, for instance, is based on the Nikkei 225 index and uses different trigger points and halt durations. European markets use variations as well, though many have adopted mechanisms broadly similar to the US model following the 2010 flash crash.

What This Means for You as an Investor

Understanding circuit breakers changes your behavior during market stress. When trading halts, resist the urge to panic-sell at the opening. Historical evidence suggests that markets tend to recover at least partially after circuit breaker triggers—the 2020 example is instructive here. The halt exists precisely because the selling pressure was irrational; once trading resumes with new information available, calmer heads often prevail.

That said, circuit breakers are a last resort, not a prevention mechanism. The real lesson for investors is that market volatility is inevitable, and circuit breakers are simply a tool to manage acute crises—not a shield against long-term drawdowns. Your portfolio should be constructed with the expectation that these halts will happen eventually, because they will. The 2020 circuit breaker activations should have surprised no one who understood market history.

What’s unresolved, and what regulators continue to debate, is whether circuit breakers as currently designed are appropriate for an era of algorithmic trading, derivative complexity, and increasingly interconnected global markets. The 2013 revisions addressed flash crash concerns, but new technologies always create new vulnerabilities. Whether the next generation of circuit breakers will look like today’s system remains genuinely uncertain.

What you can control is your preparation. Know the rules. Understand that trading halts are designed to protect the system—and potentially your portfolio—from the worst outcomes. And when the market freezes, remember: it’s doing exactly what it was built to do.