Imagine a financial system where you don’t need banks to send money, earn interest, or get a loan. No paperwork, no waiting days for approvals, and no middlemen taking a cut. This isn’t a futuristic fantasy—it’s happening right now through DeFi, short for Decentralized Finance.

DeFi is transforming how people around the world, including millions in India, access financial services. Whether you want to earn passive income on your savings, borrow money without visiting a bank, or simply understand what all the cryptocurrency buzz is about, this guide will walk you through everything in plain language.

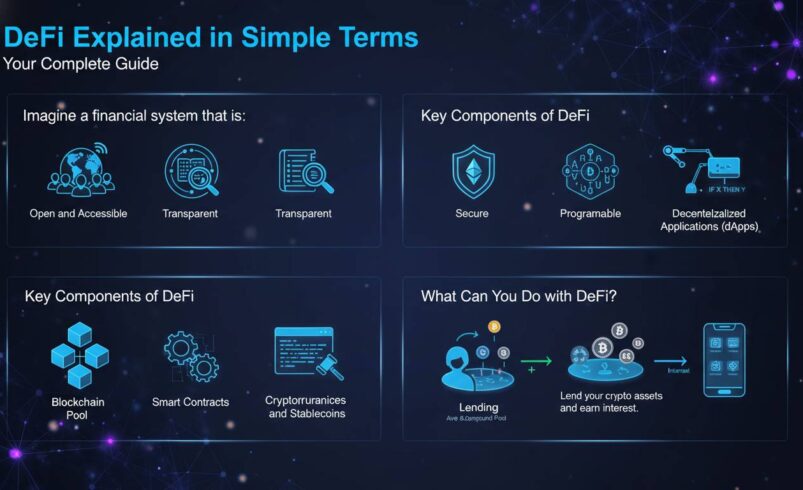

What Exactly is DeFi?

DeFi refers to financial services built on blockchain technology—same technology that powers cryptocurrencies like Bitcoin and Ethereum. The key word is “decentralized,” meaning there’s no single authority like a bank, government, or company controlling these services.

Traditional finance works like this: if you want to send money to a friend, your bank acts as the middleman. They verify the transaction, keep records, and often charge fees. If you want a loan, banks evaluate your credit history, charge interest, and hold your assets as collateral. DeFi removes these middlemen entirely.

In DeFi, “smart contracts”—self-executing code stored on the blockchain—handle everything automatically. When you lend your money through a DeFi platform, a smart contract ensures you get paid interest. When you borrow, the contract automatically releases funds once you provide collateral. No bank officers, no paperwork, no delays.

For Indians, this matters because traditional banking services remain out of reach for many. According to World Bank data, about 190 million adult Indians don’t have bank accounts. DeFi promises financial inclusion through nothing more than a smartphone and internet connection.

How DeFi Works: The Building Blocks

Understanding DeFi becomes easier when you break it into three components: blockchain, smart contracts, and decentralized applications (dApps).

Blockchain serves as the underlying technology—a shared digital ledger that records all transactions across thousands of computers worldwide. Once information enters the blockchain, it’s nearly impossible to alter, making the system transparent and secure.

Smart contracts are programs that automatically execute when predetermined conditions are met. Think of them like vending machines: insert money, select your drink, and the machine automatically delivers it. No human employee needed. In DeFi, these contracts handle interest payments, collateral releases, and trade executions instantly.

Decentralized applications (dApps) are user-friendly interfaces that connect people to DeFi services. Just as you use apps on your phone to access banking services, dApps provide the interface for interacting with DeFi protocols.

The most popular blockchain for DeFi is Ethereum, which hosts the majority of decentralized applications. Other chains like Solana, Polygon, and Avalanche have also gained significant traction, offering faster transactions and lower fees.

Major DeFi Use Cases Anyone Can Understand

DeFi isn’t just one thing—it’s an entire ecosystem of financial services rebuilt from scratch. Here are the main categories:

1. Lending and Borrowing

You can lend your cryptocurrency holdings to earn interest—often significantly higher than traditional savings accounts. Platforms like Aave, Compound, and MakerDAO allow users to deposit assets and earn variable interest rates that update in real-time.

Borrowing works similarly but inversely. You lock up collateral (usually cryptocurrency) and receive a loan in another asset. What makes this revolutionary is accessibility: you don’t need a credit score, identity verification, or geographical proximity to a bank. In India, where getting a personal loan often requires extensive documentation, DeFi offers an alternative path.

Interest rates in DeFi fluctuate based on supply and demand. When more people lend than borrow, rates drop. When borrowing demand surges, rates rise. As of recent data, stablecoin lending rates range from 3% to 8% annually, while more volatile assets can earn 10% or higher—though with corresponding risks.

2. Decentralized Exchanges (DEXs)

Traditionally, if you wanted to trade cryptocurrency, you’d use a centralized exchange like CoinDCX or WazirX in India—platforms that hold your funds and match your orders with other users. DEXs work differently: they allow peer-to-peer trading without holding your money.

When you trade on a DEX like Uniswap or Sushiswap, your funds go directly from your wallet to the blockchain, executing the trade through automated market makers (AMMs). These systems use mathematical formulas to determine prices rather than matching buyers and sellers manually.

For Indian users, DEXs offer advantages: no know-your-customer (KYC) requirements in many cases, continuous trading (24/7), and often lower fees for large trades. However, users must understand how to secure their private keys—lose those, and access to funds is gone forever.

3. Yield Farming and Staking

Yield farming involves moving your crypto assets between different DeFi protocols to maximize returns. It’s like shopping for the best interest rates across multiple banks simultaneously. You might deposit your stablecoins on one platform for 5% APY, then take the tokens you receive as rewards and stake them elsewhere for additional returns.

Staking, while related, typically involves locking up cryptocurrency to support a blockchain network’s operations. In return, stakers receive rewards. Ethereum’s transition to proof-of-stake made staking more accessible, with annual yields around 4-7% for regular stakers.

Both activities can generate impressive returns but carry substantial risks, including smart contract vulnerabilities, impermanent loss (when the value of tokens in a liquidity pool changes unfavorably), and platform failures.

4. Stablecoins

Stablecoins are cryptocurrencies designed to maintain a fixed value, usually pegged to the US dollar or Indian rupee. They provide stability in the volatile crypto markets and enable DeFi transactions without worrying about price swings.

Popular stablecoins include USDT (Tether), USDC, and DAI. For Indians, stablecoins offer a way to enter the DeFi ecosystem while minimizing exposure to cryptocurrency volatility. You can convert rupees to USDT, then use USDT across various DeFi platforms for lending, trading, or earning interest.

Why DeFi Matters Particularly for India

India presents a unique landscape for DeFi adoption. Several factors make this technology especially relevant:

The unbanked population remains substantial. DeFi requires only internet access and a cryptocurrency wallet, potentially extending financial services to rural areas where traditional banking infrastructure is limited.

Remittances represent another significant opportunity. Indians working abroad send billions of dollars home annually, with remittance fees often consuming 3-5% of the transfer value. DeFi can reduce these costs to a fraction of a percent while enabling near-instant transfers.

Young, tech-savvy population embrace new technologies readily. India ranks among the highest in cryptocurrency adoption globally, with millions actively trading and holding digital assets.

Regulatory clarity has been evolving. The Indian government has implemented taxation on crypto gains and virtual digital assets, providing some framework for legal operation—though the landscape continues developing.

Risks and Challenges You Should Know

DeFi isn’t without significant risks. Understanding these challenges is essential before participating:

Smart contract vulnerabilities remain a primary concern. While blockchain itself is secure, smart contracts are written by humans and can contain bugs. Hackers have exploited these vulnerabilities to steal billions in DeFi exploits. The Poly Network hack in 2021 saw $610 million stolen, though most was later recovered.

No consumer protection exists in DeFi. Traditional banks offer deposit insurance and fraud protection. DeFi has none. If you send funds to the wrong address or fall victim to a scam, recovery is virtually impossible.

Volatility affects everything. While stablecoins maintain their peg, the collateral you lock up to borrow can lose significant value rapidly. This can trigger liquidation—automatically selling your collateral to repay the loan.

Complexity creates barriers. Using DeFi requires managing cryptocurrency wallets, understanding gas fees (transaction costs), and navigating multiple platforms. For newcomers, the learning curve is steep.

Regulatory uncertainty persists. Governments worldwide, including India, continue debating how to regulate DeFi. Future restrictions could impact accessibility or force platform changes.

Getting Started with DeFi Safely

If you’re interested in exploring DeFi, a cautious approach protects your capital:

Start small. Begin with amounts you can afford to lose entirely. DeFi remains experimental, and even experienced users suffer losses.

Do thorough research. Before using any platform, investigate its security audits, track record, and community reputation. Search for any past exploits or controversies.

Use reputable aggregators. Platforms like Yearn Finance or Instadapp simplify DeFi by bundling multiple strategies, often with better security than individual protocols.

Consider hardware wallets. For significant holdings, hardware wallets like Ledger or Trezor provide better security than phone or browser-based software wallets.

Diversify across platforms. Don’t put all your funds in one protocol. Spreading across multiple platforms reduces exposure to any single point of failure.

The Future of DeFi: What to Expect

DeFi continues evolving rapidly. Several trends are shaping its future:

Institutional adoption is increasing. Major financial institutions are exploring DeFi for settlement, lending, and asset tokenization. This brings more capital and legitimacy but also potentially more regulation.

Cross-chain compatibility improving means users can move assets between different blockchains more easily. Bridges connecting Ethereum, Solana, and other chains expand possibilities while creating new risks.

Real-world asset tokenization brings traditional assets like real estate, stocks, and commodities onto blockchains. This could make fractional ownership and global trading more accessible.

Regulatory frameworks will likely clarify in coming years. India’s approach, in particular, could set precedents for other developing nations with large unbanked populations.

Frequently Asked Questions

What is the minimum amount needed to start with DeFi?

You can start with very small amounts—some platforms accept deposits worth just a few dollars. However, consider transaction fees (gas fees) that might make very small deposits impractical. Starting with 500-1000 INR equivalent in cryptocurrency allows you to experiment without significant risk.

Is DeFi legal in India?

As of now, cryptocurrency and DeFi activities are legal in India, though they face taxation. The government has implemented a 30% tax on crypto gains and a 1% tax deducted at source on certain transactions. However, regulations continue evolving, so staying updated on current rules is essential.

How do I keep my DeFi funds safe?

Use hardware wallets for significant holdings, enable two-factor authentication on connected accounts, never share your private keys or seed phrases, verify all transaction details before confirming, and use reputable platforms with verified smart contracts and security audits.

Can I lose all my money in DeFi?

Yes, DeFi carries substantial risk. You can lose money through hacks, smart contract failures, rug pulls (scams where developers abandon projects), market volatility, and user error. Never invest more than you can afford to lose entirely.

Do I need to be tech-savvy to use DeFi?

Some technical comfort helps, but DeFi platforms increasingly offer improved user interfaces. Understanding basic concepts like wallets, private keys, and blockchain transactions is necessary. Starting with simple lending platforms and gradually exploring more complex features as you learn is advisable.

How is DeFi different from traditional banking?

DeFi removes middlemen, operates 24/7 globally, typically offers higher interest on savings, provides faster transactions, requires no credit checks or identity verification, and offers transparency through public blockchain records. However, it lacks the consumer protections, insurance, and regulatory oversight of traditional banks.

DeFi represents a fundamental shift in how financial systems can operate—more accessible, transparent, and efficient for many, while introducing new risks unfamiliar to traditional finance. For Indians seeking alternatives to conventional banking or exploring ways to put cryptocurrency holdings to work, understanding DeFi opens doors to a rapidly growing ecosystem. Start small, learn continuously, and never invest more than you can afford to lose.