The first biotech stock I ever bought was a disaster. I was drawn in by headlines about a revolutionary cancer treatment, poured my savings in based on a press release, and watched half my money disappear when the Phase 2 trial failed. That experience taught me something nobody in the industry talks about openly: you don’t need to understand molecular biology to lose money in biotech, but you absolutely need a financial framework to survive it.

What followed was a decade of studying how institutional investors evaluate these companies. I discovered that the best biotech analysts on Wall Street aren’t necessarily the ones who understand drug chemistry — they’re the ones who know how to read a balance sheet, assess clinical risk, and spot dilution before it destroys shareholder value. This guide distills that knowledge into a practical toolkit you can use starting today.

Focus on the Business Model, Not the Molecule

Here’s the uncomfortable truth: the actual science behind a drug candidate matters far less for your investment decision than you think. A brilliant molecule means nothing if the company can’t execute, if the market opportunity is overstated, or if management dilutes shareholders into oblivion.

The question you should be asking isn’t “Will this drug work?” — that’s a question for the FDA and the scientists who design the trials. The question you should be asking is “Can this company survive long enough to find out if the drug works?”

Biotech companies are fundamentally different from most publicly traded businesses. A restaurant chain or software company can generate revenue while you figure out its long-term strategy. Most biotech companies have zero revenue, burning cash every month, and are betting everything on a handful of clinical trials that may take years to complete. Your job as an investor is to determine whether the company has enough runway to reach the next catalyst — whether that’s a trial readout, a partnership announcement, or an FDA approval.

This shift in mindset is the foundation of everything that follows. You’re not evaluating a product; you’re evaluating a financial vehicle designed to de-risk a scientific hypothesis over time.

The Five Metrics That Actually Matter

When I first started analyzing biotech stocks, I made the mistake of spending hours reading clinical trial protocols and scientific publications. I was trying to become a scientist. That was a waste of time. What actually moved the needle was mastering a handful of financial metrics that Wall Street uses to value these companies. Here are the five I check first on any biotech investment.

Cash Runway: This is your most important number. Calculate how many quarters of cash the company has left by dividing its cash position by its quarterly burn rate. If a company has $50 million in cash and burns $10 million per quarter, it has five quarters of runway. You want companies with at least four quarters of cash — anything less than that, and you’re gambling on a financing that will likely dilute your shares. As of early 2025, the median biotech company carries roughly 2.5 years of cash, though early-stage developers often have less.

Market Cap vs. Cash: Take the company’s market cap and subtract its cash position. This gives you the “enterprise value” stripped of its cash pile. If a company has a $500 million market cap but $200 million in cash, the market is valuing its operations at $300 million. Now ask yourself: is that valuation reasonable given the pipeline? This metric becomes especially important when evaluating companies with upcoming trial readouts — if the market cap is barely above cash, the market may be signaling that it doesn’t believe in the pipeline at all.

Pipeline Value: This is harder to quantify, but you can estimate it by looking at what comparable companies have been acquired for. If a company in Phase 2 for a specific indication was acquired for $2 billion, and your target company is in Phase 1 for the same indication, you can use a discount model to estimate potential value. The key is to find comparable transactions — recent deals in the same therapeutic area give you the best reference points. Biotech M&A activity in 2023-2024 has been selective, with large pharma companies focusing on late-stage assets, which means early-stage pipeline valuations have compressed.

Price-to-Sales Ratio: Unlike traditional P/E ratios, which are useless for pre-revenue companies, P/S gives you a way to compare valuations. A biotech company with a $1 billion market cap and $100 million in annual grant or partnership revenue trades at 10x sales. Whether that’s expensive depends on the pipeline, but at least you have a number to work with. For reference, the average biotech trades between 3x and 8x sales, with premium valuations reserved for companies with late-stage programs.

Insider and Institutional Ownership: Track what insiders are doing with their shares. If the CEO and CFO are buying in the open market, that’s a signal they believe in the story. If they’re selling, run the other direction. Similarly, look at which institutional investors hold the stock — if respected healthcare-focused funds like Baker Brothers or RA Capital have built positions, that’s a stamp of credibility. You can find this data on any major financial data provider.

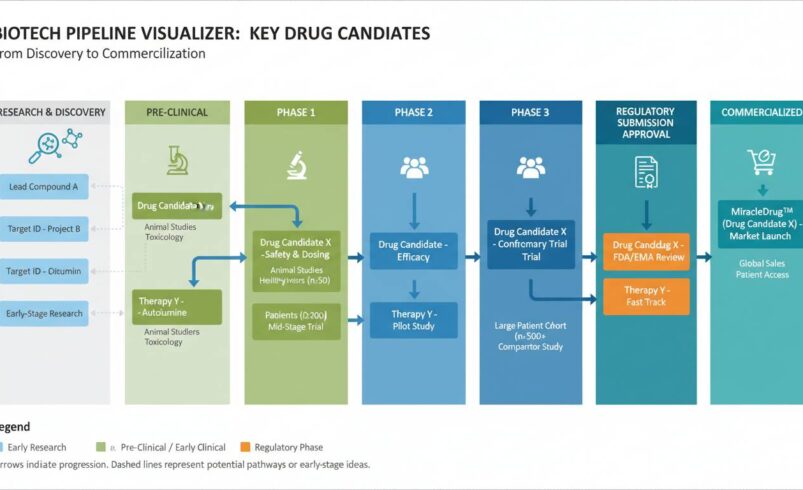

Understanding Clinical Trials Without the Science

You don’t need to know what a kinase inhibitor does to evaluate a biotech stock. What you need to understand is the clinical trial phase structure and what each stage means for the company’s timeline and valuation.

Phase 1 is about safety. The company tests the drug in a small group of healthy volunteers or patients to determine if it’s tolerable. Success here doesn’t mean the drug works — it means people don’t die from taking it. Roughly 70% of drugs move from Phase 1 to Phase 2. At this stage, the company’s value is largely speculative, driven by scientific hypothesis rather than clinical data.

Phase 2 is about efficacy. The company tests the drug in a larger group of patients to see if it actually works for its intended indication. This is where most biotech stocks make or break. A successful Phase 2 readout can send a stock up 100% or more. A failure can cut the stock in half overnight. The key question to ask: what is the comparator arm in this trial? If the control group is getting a placebo and the treatment group shows meaningful improvement, that’s a strong signal. If the comparator is an existing approved drug, you’ll want to see non-inferiority or superiority data.

Phase 3 is the definitive test. These are large-scale trials designed to confirm efficacy and monitor adverse reactions across a diverse population. Success in Phase 3 typically leads to an FDA approval application. Companies with Phase 3 programs are significantly de-risked compared to earlier-stage peers, which is why they command premium valuations.

FDA Review after Phase 3 approval can take 6-12 months. The FDA can approve, reject, or request additional studies. Even after a successful Phase 3 trial, there’s a non-trivial chance of a CRL (Complete Response Letter) requiring more work. This is why many investors sell on Phase 3 success — the binary event of FDA approval is already priced in, and any delay or complication creates downside.

The counterintuitive insight here is that you often don’t need to understand the clinical data at all to make money. What matters is understanding what data is coming, when it’s coming, and how the market has priced the probability of success. A mediocre drug that exceeds low expectations can rally harder than a strong drug that was overhyped.

Red Flags That Should Make You Walk Away

I’ve seen retail investors lose millions because they fell in love with a company’s science and ignored warning signs that were visible in plain sight on any SEC filing. Here are the red flags I never ignore.

Consistent Share Dilution: If a company has raised money through stock offerings in three of the last five years, that’s a pattern, not an exception. Check the historical share count — if it has doubled or tripled over five years, even successful trial outcomes may not generate returns for early shareholders. I look for companies where management has demonstrated financing discipline, raising money at higher valuations rather than down rounds at any available price.

Management Turnover: A revolving door in the C-suite is a sign something is wrong. If the CEO, CFO, or Chief Medical Officer has left within the past 12 months, dig into why. Was it for personal reasons, or did they see problems ahead? You can find this information in 8-K filings and earnings call transcripts.

Aggressive Partnership Terms: Companies often announce partnerships with larger pharma companies as validation. Read the fine print. If the big pharma partner has an option to acquire the drug at a deep discount to future market value, or if the royalty rates are thin, the partnership may be worth less than the headline suggests. The terms of deals announced in 2023 and 2024 have become more investor-friendly as large pharma competes for late-stage assets, but always read the 8-K.

Lack of Institutional Ownership: If no respected healthcare funds hold the stock, ask yourself why. The institutional investors who cover biotech have access to management, to scientific advisors, and to due diligence that you don’t. Their absence is often a signal that something is wrong.

The Tools You Need to Do This Yourself

You don’t need a Bloomberg terminal or Wall Street connections to evaluate biotech stocks like a pro. Most of what you need is available for free online.

SEC EDGAR is your best friend. Every public company files 10-Ks, 10-Qs, 8-Ks, and prospectuses here. The 10-K gives you the comprehensive view of the business, including risk factors that management wants you to know about. The 10-Q gives you quarterly updates. The 8-K tells you about material events — including leadership changes, financing rounds, and clinical trial updates. Make a habit of reading the 10-K risk factors section in full — it’s the most honest assessment of what could go wrong.

ClinicalTrials.gov is the government’s database of all registered clinical trials. You can look up any company and see exactly what trials are ongoing, what phase they’re in, and when they’re expected to complete. This is how you build a catalyst calendar. When a company announces a trial readout, check this database to see if the expected completion date lines up with the announcement.

Seeking Alpha and Yahoo Finance both offer company-specific news, transcript analysis, and community discussion. The articles and transcripts are more useful than the message boards. Look for write-ups from users with track records in the biotech space — some of the best due diligence I’ve seen has come from pseudonymous authors who specialize in specific therapeutic areas.

The FDA’s Drugs@FDA database lets you look up approval history, review letters, and label information for any approved drug. This is useful when evaluating companies with products already on the market or in late-stage development — you can see exactly what the FDA has approved and what conditions were attached.

Building Your Own Evaluation Framework

Now that you have the tools and the metrics, here’s how to put them together into a practical evaluation process that takes about 30 minutes per company.

First, check the cash runway. If the company has less than four quarters of cash, note that as a concern and factor in potential dilution. Second, look at the clinical trial pipeline and build a timeline of expected data readouts over the next 12-18 months. These are the binary events that will move the stock. Third, estimate pipeline value by looking at comparable M&A transactions — what have similar companies been acquired for at similar stages?

Fourth, check the institutional ownership. If respected healthcare funds hold meaningful positions, that’s a positive signal. Fifth, review management’s track record with share issuance — have they been disciplined or aggressive? Finally, check the recent news and understand the current story the market is pricing in. Is the stock up 50% on hope for a trial result? If so, you may be too late.

This framework won’t make you right every time — nothing can — but it will keep you from making the catastrophic mistakes that wipe out retail investors in this sector. The goal isn’t to pick winners; it’s to avoid the obvious losers and let winners ride.

Why This Approach Works (And Where It Fails)

The framework I’ve described works well for evaluating mid-stage and late-stage biotech companies with clear clinical catalysts. It fails when applied to early-stage companies where the science is genuinely speculative and any financial metric is a guess.

If a company is in Phase 1 with a single asset and no revenue, you’re essentially betting on the science. The financial framework I described won’t help you much because there’s no revenue to value, no comparable acquisitions to reference, and no institutional coverage to lean on. In those cases, you either need scientific expertise or you need to acknowledge that you’re gambling. There’s nothing wrong with gambling — just be honest with yourself about what you’re doing.

The other place this framework fails is in companies with platform technologies — businesses that can apply their underlying science to multiple drug candidates across different indications. These are harder to value because the pipeline is wider and the comparison to single-asset companies doesn’t work. Platform companies often trade at premiums because of optionality, but that optionality is only valuable if management executes across multiple programs.

The Bottom Line

You don’t need a biochemistry degree to invest in biotech. You need discipline, a framework, and the honesty to acknowledge what you don’t know. Focus on cash runway, clinical catalysts, institutional credibility, and management track record. Use the free tools available to you. Build a process and stick to it.

The biotech sector will continue to produce both enormous winners and spectacular losers. Your job isn’t to predict which category a company will fall into — it’s to make informed bets where the odds are in your favor and to manage your risk when the data doesn’t support the thesis.

If you’re still trying to read scientific papers to find the next big drug, stop. The professionals who do that for a living have more time, more expertise, and better information than you will ever have. What you have is the ability to analyze financial statements, assess risk, and think independently about valuation. Use that advantage.