Most people underestimate how complicated life insurance can get until they actually try to buy it. I spent fifteen years in the insurance industry, and the number of times I’ve sat across from a prospective client who thought they understood term life insurance—only to discover they’d been looking at the wrong product entirely—is staggering. The confusion isn’t entirely their fault. The insurance industry has a remarkable talent for making straightforward concepts sound like rocket science.

Term life insurance is actually simple. The confusion comes from not knowing what questions to ask, how much coverage you actually need, and why the answer matters more than most financial decisions you’ll make. This guide cuts through the noise. I won’t pretend there’s one perfect answer for everyone, but I can show you exactly how to find yours.

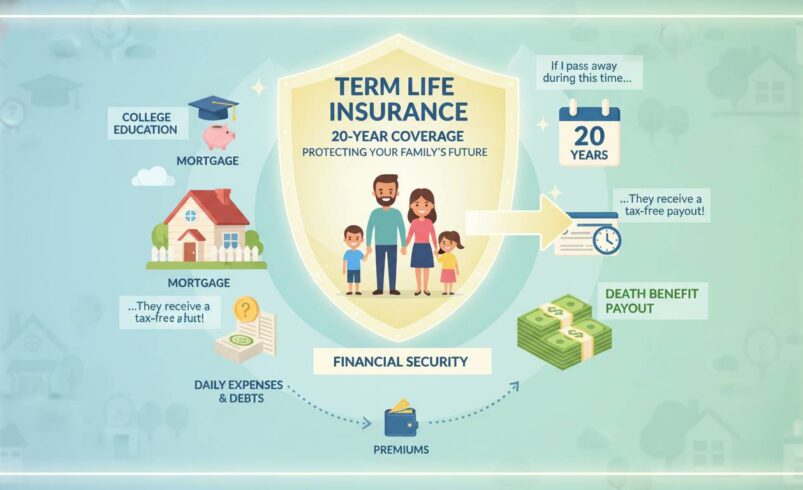

What Term Life Insurance Actually Is

Term life insurance is a contract between you and an insurance company. You pay premiums—typically monthly or annually—and in exchange, the company pays a death benefit to your designated beneficiaries if you die while the policy is active. That’s it.

What makes term life different from other life insurance types is the “term” part. These policies exist for a specific period: 10, 15, 20, 25, or 30 years are the most common options. Some insurers offer terms as short as five years or as long as 40. If you outlive the term, the policy expires. You get nothing back. No cash value, no payout, no resurrection of premiums you paid over two decades.

This is why term life costs less than permanent alternatives like whole life or universal life. You’re essentially renting coverage for a set period rather than building an investment vehicle that lasts your entire life. The insurance company knows they might never pay out—depending on when you die relative to your policy’s expiration—and they price accordingly.

The death benefit is typically a lump sum paid to your beneficiaries tax-free. They can use that money for anything: paying off the mortgage, covering college tuition for your children, replacing your income, or handling funeral expenses. The flexibility is a strong feature.

How Term Life Insurance Works

The mechanics are straightforward, but understanding the nuances matters enormously when you’re comparing policies.

When you apply for term life insurance, the insurer evaluates your health through a process called underwriting. This typically includes a medical exam (though some policies offer “no exam” options at higher costs), review of your medical history, and assessment of lifestyle factors like smoking status, occupation, and hobbies. Based on this evaluation, the company places you in a health classification—Preferred Plus, Preferred, Standard, or Substandard—with each tier affecting your premium.

Your premium stays level for the entire term if you choose a “level term” policy. This is the most common type and the one most financial advisors recommend. Your payments won’t increase as you age or if your health declines, which provides crucial budgeting stability. Some older policies feature “annual renewable term” structure where premiums start lower but increase each year—a trap that catches people who don’t read the fine print.

The policy’s “conversion” feature deserves your attention. This allows you to convert all or part of your term coverage to a permanent policy without a new medical exam, regardless of your health at conversion time. Not all policies include this, and those that do typically limit conversion to a specific window—often the first five to ten years of the policy. If your health takes a turn and you’re stuck with expiring term coverage, conversion could be your lifeline.

Beneficiary designation is equally important. You can name one or multiple beneficiaries, specify percentages, and even name a contingent beneficiary who receives the money if your primary beneficiary predeceases you. Many people name their spouse as primary beneficiary and their children as contingent, but your situation might call for something different. Life changes—divorce, death, birth of children—should trigger a review of your beneficiary designations.

Types of Term Life Insurance Policies

Not all term policies are created equal. Understanding the distinctions helps you choose the right structure for your situation.

Level term is the gold standard for most buyers. Your death benefit and premium remain constant throughout the policy period. A 30-year-old non-smoker buying a 20-year level term policy at $500,000 will pay roughly the same premium in year twenty as they paid in year one. This predictability makes financial planning easier and protects you against premium increases that could become unaffordable later.

Decreasing term policies pay out less over time. The premium stays level, but the death benefit shrinks—often in sync with a mortgage balance. These made sense when mortgages were typically 15-year instruments, but with 30-year mortgages now standard, the math rarely works out favorably. You’re usually better off with level term and investing the difference.

Return of premium term life refunds all your premiums if you outlive the policy. On paper, this sounds appealing—you can’t lose! In practice, these policies cost 50% to 100% more than standard term policies. You’d almost always come out ahead investing the difference in a simple index fund, but these products sell well to people who dislike the idea of “losing” their premium payments.

Annual renewable term starts with low premiums that increase every year. Insurers bet that most people will either die (triggering a payout) or drop the policy before age-related premium jumps become painful. These policies can work for short-term needs—covering a business loan during a specific project, for instance—but are terrible for long-term planning.

The choice typically comes down to level term. Everything else involves trade-offs that rarely benefit the buyer.

How Much Term Life Insurance Coverage You Need

This is the question that keeps people up at night, and the one where generic advice fails most spectacularly. I’ll give you a framework for thinking through this, because the right answer depends entirely on your circumstances.

The simplest starting point uses the “DIME” formula: Debt, Income, Mortgage, Education.

Debt includes everything you’d leave behind: credit card balances, auto loans, personal loans, and any other debts that wouldn’t die with you. Add up the total.

Income replacement typically uses a multiplier—financial advisors often suggest 10 to 12 times your annual income. This provides a pool that, when invested conservatively, can replace your income indefinitely. Alternatively, calculate the number of years until retirement and multiply your annual income by that figure. A 35-year-old earning $75,000 with 30 years until retirement might want $2.25 million in coverage just for income replacement.

Mortgage balance gets added to whatever figure you reach. If you owe $300,000 on your home, that goes in the calculation.

Education costs for children—college tuition and expenses—typically run $100,000 to $200,000 per child at current prices. Include this if you plan to help fund their education.

This approach gives you a rough number, but it has limitations. It doesn’t account for your spouse’s income, existing savings, life insurance through employment, or whether your children will need support for two years or twenty. These factors significantly impact the right answer.

A more personalized approach asks what financial goals you’d want to achieve if you died tomorrow. List them specifically: “pay off the house,” “fund four years of college for both kids,” “leave my spouse enough to not work for five years.” Add up the price tags. That’s your coverage target.

Factors That Determine How Much Coverage You Need

Beyond the basic DIME calculation, several factors should adjust your target number up or down.

Your spouse’s income and earning potential dramatically affects the calculation. A high-earning spouse with excellent career prospects needs less replacement income than someone supporting a family on a single income with limited employment options. Dual-income households often need less coverage than single-income households, all else equal, because the surviving spouse can maintain their standard of living more easily.

Existing life insurance through employer benefits might already cover a significant portion of your needs. Many employers provide one to two times your salary in free life insurance, with options to purchase additional coverage at group rates. Group coverage has limitations—it’s typically not portable if you change jobs, and the amount rarely scales with your actual needs—but it should factor into your calculation.

Savings and investments that your family could access matter. A substantial retirement account, taxable investments, or real estate equity reduces the amount of life insurance you need to replace your income. However, some of these assets might be better left invested for your family’s long-term security rather than liquidated at death.

The ages of your children directly correlate with how long they’ll need financial support. A newborn needs support for potentially 22+ years until financial independence. A 16-year-old needs support for perhaps six years. The math differs substantially based on age.

Your retirement timeline affects the calculation in two ways. First, if your children are approaching independence and your mortgage will be paid off before retirement, your coverage needs might drop substantially over time. Second, if you’re planning to support yourself in retirement through savings rather than Social Security or pension, your spouse might need additional coverage to maintain that plan if you die first.

Calculating Your Specific Coverage Amount

Rather than relying on rules of thumb, building a custom calculation serves you better. I’ll walk through a practical example.

Meet Alex, 38 years old, married to Jamie, also 38. They have two children: a 6-year-old and a 3-year-old. Alex earns $95,000 annually; Jamie earns $70,000. Their mortgage balance is $340,000 with 27 years remaining. They have $45,000 in combined student loans, $8,000 in car loans, and $15,000 in credit card debt. They want to help both children attend a four-year college.

Step one: Debt replacement. $45,000 + $8,000 + $15,000 = $68,000.

Step two: Mortgage payoff. Add $340,000. Total so far: $408,000.

Step three: Income replacement. If Jamie continues working, they might need 50% to 75% of Alex’s income replaced rather than 100%. However, childcare costs would increase significantly if Jamie became the sole parent. Let’s estimate Alex’s income replacement at 75% for 15 years (until the younger child reaches 18): $95,000 × 0.75 × 15 = $1,068,750. Running this number through a present-value calculation at a 3% assumed return rate yields roughly $870,000 in needed coverage.

Step four: Education. At $150,000 per child for four-year degrees: $300,000.

Total estimated need: $408,000 + $870,000 + $300,000 = $1,578,000.

This number might feel overwhelming, but remember: this is the total needed to fully replace Alex’s financial contribution across all dimensions. Many families would adjust this downward based on what they believe is realistic. Some families would carry significantly more life insurance during the peak-need years and allow coverage to decrease as children become independent and debts are paid.

Common Mistakes When Buying Term Life Insurance

After years of reviewing policies and claims, I’ve seen the same errors repeat themselves. Avoiding these mistakes saves money and prevents coverage gaps when they matter most.

Buying the wrong term length is the most common error. A 30-year term might seem conservative, but if you’re 45 when you buy it, you’ll be 75 when it expires—with no coverage when you might need it most. Conversely, a 10-year term for a 30-year-old parent leaves coverage expiring just as children reach college-age peak expenses. Match your term to your longest anticipated need.

Skipping the conversion option to save premium dollars costs people dearly. If your health declines during your term, you might be uninsurable when you want to convert. The small premium increase for conversion rights pays for itself if your health changes.

Not comparing insurers costs you significantly. Each insurer prices risk differently. A 40-year-old male in excellent health might pay $800 annually for a 20-year, $500,000 policy with one company and $1,200 with another. Over the policy lifetime, that’s $8,000 to $16,000 in unnecessary payments. Always get quotes from at least four or five insurers.

Ignoring policy riders can leave gaps in your coverage. Disability waiver of premium (waives premiums if you become totally disabled), accelerated death benefit (allows access to part of your benefit if you’re diagnosed with a terminal illness), and child rider (provides small coverage for each child) might be worth the additional cost depending on your situation.

Underestimating future needs leads to being underinsured. People buy based on their current situation without accounting for career growth, additional children, or lifestyle changes. Building some buffer into your coverage or planning for policy increases later (through guaranteed insurability riders) helps address this.

How to Choose the Right Term Life Policy

Finding the right policy combines practical steps with strategic thinking about your long-term situation.

Start with online comparison tools—sites like Term4Sale, Policygenius, or Quotacy provide quotes from multiple insurers without requiring personal information beyond basic demographics. These aggregators don’t include every insurer, but they cover the major players and give you a sense of the price range. Expect to see variations of 30% to 50% between the cheapest and most expensive offers for the same coverage.

Once you have a target price range, narrow down to the insurers offering the best rates in your health category. Then dig into policy details: conversion windows, rider options, the insurer’s financial strength rating (AM Best, Standard & Poor’s, or Moody’s), and customer service reputation. A slightly more expensive policy from a company with superior financial strength and conversion options often makes more sense than the cheapest option.

The application process for term life typically takes 20 to 30 minutes for a straightforward case. You’ll answer questions about your health history, family medical history, driving record, occupation, and hobbies. The medical exam—usually done at a local clinic and paid for by the insurer—takes another 30 minutes and includes blood work, urine sample, height/weight, and blood pressure reading.

Approval times vary from “instant” for the healthiest applicants to four to six weeks for more complex cases. If you need coverage quickly for a mortgage or other time-sensitive matter, mention this to the insurer; some offer expedited underwriting for an additional premium.

Term vs. Whole Life: When Permanent Coverage Makes Sense

The comparison comes up constantly, so I’ll address it directly: most people need term life, not whole life.

Whole life insurance combines death benefit protection with a cash value component that grows tax-deferred. Premiums are substantially higher—often five to ten times the cost of term coverage for the same death benefit. The cash value grows slowly in the early years and only becomes meaningful after a decade or more.

For most families, the math doesn’t work. You’d be better served by buying term coverage and investing the premium difference in low-cost index funds. A 35-year-old buying $500,000 of 20-year term might pay $400 annually while the equivalent whole life premium could run $3,500. Investing that $3,100 annual difference in an S&P 500 index fund would likely yield substantially more than the whole life cash value over twenty years.

However, permanent coverage makes sense in specific situations. High-net-worth individuals might use whole life for estate planning purposes, leveraging the death benefit to pay estate taxes. Business owners sometimes use permanent policies for key person insurance or buy-sell arrangements. People with medical conditions that would make future term coverage impossible might lock in permanent coverage while they’re still insurable.

For everyone else—and that’s the vast majority of people—term life provides the protection needed at a price that makes financial sense.

Practical Tips for Buying Term Life Insurance

Moving from understanding to action requires knowing how to navigate the purchase process efficiently.

Apply sooner rather than later. Your health can only deteriorate, and premium rates increase with age. A healthy 30-year-old might pay $30 per month for $500,000 of 20-year term; the same policy at age 40 might cost $50, and at age 50 might cost $120. Waiting costs money.

Don’t overbuy coverage. More coverage means higher premiums, and money spent on unnecessary coverage could go toward retirement savings or paying down debt. Use the calculation framework from earlier to arrive at a target number, then round to a convenient level—often $500,000 or $1,000,000 increments.

Consider a term that peaks with your needs. If your youngest child is three now and you’d like coverage through their college graduation (approximately 15 years), a 20-year term provides five years of buffer while remaining affordable.

Review employer options before buying individually. Many employers offer supplemental life insurance that you can buy without medical exam, up to certain amounts. This coverage is often portable (you can take it with you if you leave), though premiums typically increase after separation from employment. Employer coverage can serve as a supplement to individually-purchased coverage.

Work with an independent agent if you want guidance. Unlike captive agents who represent one insurer, independent agents represent multiple companies and can shop on your behalf. They typically don’t charge a fee—the commission is built into the premium—and can help you navigate medical requirements, policy options, and underwriting nuances.

What Remains Unresolved

The honest admission I owe you is this: there’s no perfect formula for determining exactly how much term life insurance you need. The calculation involves assumptions about inflation, investment returns, your career trajectory, your spouse’s earning ability, and how long your children will need support. Anyone who tells you they have the precise answer is selling something.

What you can do is build a reasonable estimate using the framework above, add a margin for error, purchase coverage that fits your budget, and commit to reviewing your situation every three to five years—or whenever a major life event occurs. Your needs will change. Your coverage should too.

The right amount of term life insurance isn’t a number you find once and forget. It’s a number you arrive at through thoughtful calculation, then manage as your life evolves.