Most people understand saving money is wise. What fewer grasp is why a single dollar invested at age 25 could outperform decades of aggressive saving by someone who starts at 35. The mechanism behind this counterintuitive reality is compound interest, and once you see how it works, you’ll understand why Albert Einstein allegedly called it the eighth wonder of the world. The attribution is disputed—there’s no verified record of Einstein saying exactly that—but the sentiment captures something real: compound interest possesses a mathematical power that seems almost magical until you understand the engine driving it.

Understanding Compound Interest: More Than Just “Interest on Interest”

Compound interest is interest calculated on both the initial principal and the accumulated interest from previous periods. That’s the textbook definition, and it misses the visceral impact of what actually happens when you let this process run.

When you deposit $1,000 in an account earning 5% compound interest annually, you earn $50 in the first year. In year two, you earn interest on $1,050—not just your original $1,000. The interest itself begins generating returns. Over time, this creates an accelerating curve that bends upward in ways linear thinking simply cannot predict.

The key distinction lies in what economists call the time value of money. A dollar today is worth more than a dollar tomorrow because that dollar can start working immediately. Compound interest is the mechanism that transforms this abstract principle into concrete wealth—or, if you’re on the borrowing side, concrete debt.

The formula itself is straightforward: A = P(1 + r/n)^(nt). But the numbers it produces are anything but simple. Understanding this formula and its implications requires seeing it in action, which is where most financial education falls short.

The Compound Interest Formula: Breaking Down the Mathematics

The standard compound interest formula contains five variables, and each one determines your outcome.

A represents the final amount. P is your principal, the initial sum you’re investing or borrowing. The variable r stands for your annual interest rate expressed as a decimal, so 5% becomes 0.05. The letter n indicates how many times interest compounds per year—daily compounding uses 365, monthly uses 12, annually uses 1. Finally, t represents the number of years the money compounds.

Here’s where intuition usually fails. Most people assume that doubling your interest rate doubles your returns. It doesn’t. Doubling your time horizon, however, produces returns that seem impossible until you’ve done the math.

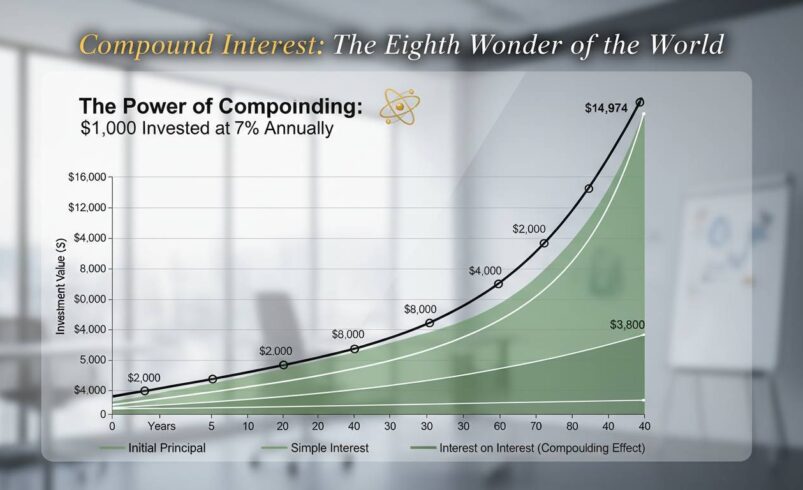

Consider $10,000 invested at 7% annual interest. After 30 years using annual compounding, you have $76,122.55. The math: 10,000 × (1.07)^30. Your money multiplied more than 7.6 times, but you contributed nothing after the initial deposit. Now extend that to 40 years: $149,744.58. Ten additional years—roughly a third more time—nearly doubled your final amount.

This is the formula’s secret. The exponent does the heavy lifting, and exponents reward patience with geometric, not arithmetic, growth.

Simple Interest vs. Compound Interest: The Gap Widens Dramatically

Simple interest calculates returns only on the original principal. If you have $10,000 at 7% simple interest for 30 years, you earn $700 annually for a total of $21,000 in interest plus your principal, ending with $31,000.

The same $10,000 at 7% compound interest, as calculated above, gives you $76,122.55. The difference—$45,122.55—represents the interest on interest that compound returns generate. More than double the final amount from the exact same starting point, the exact same rate, just a different calculation method.

This gap shrinks dramatically over short timeframes. Over one year, simple and compound interest at the same rate produce identical results. Over five years, the difference is noticeable but manageable. Over twenty or thirty years, the gap becomes enormous.

The practical implication is straightforward: when evaluating any financial product, always ask how interest compounds. A savings account advertised at 4% that compounds daily will outperform one at 4.5% that compounds annually, given enough time. The math isn’t intuitive—most people guess wrong on this—which is precisely why understanding the difference matters.

Real-World Examples: What Compound Interest Actually Produces

The S&P 500 has returned approximately 10% annually on average over the past century before inflation. While past performance doesn’t guarantee future results, using this historical benchmark illustrates compound interest’s power.

If you invested $500 monthly starting at age 25 until age 65 (40 years), at 10% annual returns, you’d contribute $240,000 of your own money. Your portfolio would be worth approximately $1.77 million. Your contributions represent less than 14% of the final amount. The rest—$1.53 million—came from compound returns.

Now compare someone who waits until 35 to start investing the same $500 monthly until age 65. They contribute $180,000 (30 years × 12 months × $500). Their portfolio reaches approximately $611,000. They invested 25% less of their own money but ended up with 65% less wealth. The ten-year delay cost them over $1.1 million in potential returns.

On the debt side, credit card companies exploit compound interest with ruthless efficiency. Carrying a $5,000 balance at 24% APR, compounded daily, costs roughly $1,200 in interest during the first year alone. Minimum payments that cover only interest—never touching the principal—can trap borrowers indefinitely. Someone making $50 monthly payments on that $5,000 balance would need over 29 years to pay it off and would fork over more than $12,000 in total payments.

These examples aren’t hypotheticals. They’re the mathematical inevitabilities that compound interest produces, whether you’re the one earning it or paying it.

Why It’s Called the Eighth Wonder: The Origin and Meaning

The phrase “compound interest is the eighth wonder of the world” appears everywhere from financial blogs to motivational speeches, always attributed to Einstein, rarely with evidence.

The attribution is likely apocryphal. No credible historical record places these words in Einstein’s mouth. He certainly discussed compound interest—he taught physics at Princeton and wrote about exponential growth—but the specific quote appears to be a 20th-century invention that gained momentum through repetition.

Regardless of its origin, the phrase survives because it captures something true: compound interest produces results that seem to violate normal expectations. Linear thinkers—most humans by default—struggle to internalize how dramatically exponential functions behave. We underestimate how much time compounds, and we underestimate how much small differences in rates or timeframes compound into massive outcome differences.

This is why the phrase resonates across cultures. Similar attributions appear linking the quote to Keynes, to unnamed rich fathers, to various financial gurus. The message matters more than the messenger. Compound interest possesses a power that, once witnessed, feels almost too good to be true—which is exactly what “eighth wonder” conveys.

The Rule of 72: A Shortcut That Reveals Compound Interest’s Power

If you remember only one shortcut from this article, make it the Rule of 72.

Divide 72 by your annual interest rate, and the result tells you approximately how many years it takes for your money to double. At 6% annual returns, money doubles in about 12 years (72 ÷ 6 = 12). At 8%, it doubles in roughly 9 years. At 4%, approximately 18 years.

This isn’t precise mathematics—it’s an approximation that works remarkably well for rates between 2% and 10%. But its value lies in forcing intuitive understanding of exponential growth.

Using this rule, you can immediately see that money at 6% takes about 12 years to double, 24 years to quadruple, and 36 years to become eight times larger. This is why starting early matters so enormously. A 25-year-old with $10,000 at 7% has approximately $80,000 by age 55—not because they worked for it, but because the math did.

The Rule of 72 also works inversely for debt. At 18% APR on a credit card, your balance doubles in approximately 4 years (72 ÷ 18 = 4). This perspective changes how you view high-interest debt. It’s not just expensive—it’s exponentially destructive.

The Frequency of Compounding: Why Daily Beats Annual

The formula includes n—the number of compounding periods per year—because it dramatically affects outcomes, especially over longer timeframes.

Daily compounding (n = 365) produces more money than monthly (n = 12), which produces more than annual (n = 1), at the same APR. The differences seem small individually, but they accumulate.

On $100,000 at 5% for 30 years, annual compounding yields $432,194. Monthly compounding yields $448,923. Daily compounding yields $454,595. The difference between annual and daily compounding—$22,401—is larger than the original principal.

When choosing accounts or evaluating loans, always check the compounding frequency. Banks advertise APR but compound interest differently. Two loans with identical 6% APR can carry dramatically different effective rates depending on how interest accrues. APR doesn’t tell the whole story.

For investments, daily or monthly compounding is typically standard. For loans, especially some payday loans and subprime auto loans, aggressive daily compounding can make them far more expensive than surface rates suggest.

The Dark Side: How Compound Interest Works Against You

Every dollar that compound interest produces for savers, it extracts from borrowers. Understanding this symmetry is crucial for financial literacy.

Mortgages illustrate this clearly. A $300,000 mortgage at 6.5% for 30 years results in total payments of approximately $683,000—more than double the original loan amount. The $383,000 in interest represents compound working against you, month after month, for three decades.

Student loans present similar dynamics. The average federal student loan interest rate hovers around 5-6%, but capitalized interest—unpaid interest that gets added to principal—can cause balances to grow during deferment periods. Someone graduating with $35,000 at 6% who defers payments for two years while interest capitalizes might see their balance grow to $37,000 before they even make their first payment. That $2,000 didn’t buy anything. It came purely from compound interest working against them.

The psychologically painful reality is that compound interest punishes procrastination for borrowers much more severely than for savers. Missing a credit card payment triggers penalty rates that can jump from 15% to 25% overnight. That higher rate then compounds on a larger balance, creating a feedback loop that traps people deeper in debt.

Limitations and Counterintuitive Truths About Compound Interest

Here’s what most articles on this topic won’t tell you: compound interest works, but expectations need calibration.

First, the 7% average annual return that financial calculators default to isn’t guaranteed. The stock market’s long-term average includes devastating crashes—the Great Depression, the 2000 dot-com bust, the 2008 financial crisis. People who sold during panics didn’t experience 7% returns. Real returns, after inflation, run closer to 5% historically. This doesn’t invalidate compound interest, but it does mean projections should include realistic assumptions rather than optimistic ones.

Second, compound interest requires consistency to work. The mathematical models assume continuous compounding without interruption. In reality, life intervenes. Medical emergencies, job losses, market crashes—these disrupt the steady compounding that produces magical results. Someone who stops contributing during a recession and restarts years later loses the exponential benefit of those missing years.

Third, and most importantly, compound interest’s power depends entirely on returning to a zero-based starting point. $10,000 at 7% for 30 years becomes $76,000. But if you withdraw your gains each year, you end with $10,000 plus $2,100 in annual interest ($63,000 total), not $76,000. The magic requires leaving returns invested. This sounds obvious stated plainly, but behavioral finance shows that most investors—professionals included—struggle to leave winners alone. We take profits. We diversify too early. We interrupt the very process that creates wealth.

These limitations aren’t reasons to dismiss compound interest. They’re reasons to understand it clearly, plan for the disruptions, and design systems that let compounding continue uninterrupted.

How to Use Compound Interest to Your Advantage

The strategies for harnessing compound interest are straightforward. Execution matters more than creativity.

First, start immediately. The mathematical advantage of starting at 25 versus 35 cannot be overstated. Someone who invests $200 monthly from age 25 to 35 (10 years) then stops contributing will have more money at age 65 than someone who invests $200 monthly from 35 to 65 (30 years). The early starter contributed $24,000 total. The later starter contributed $72,000. Yet the early starter ends with more money because they gave compound interest more time to work.

Second, automate your contributions. Treat savings like a bill that must be paid. 401(k) contributions deducted automatically from payroll, mutual fund purchases scheduled for the day after your paycheck—these systems remove decision fatigue and ensure consistent compounding.

Third, reinvest dividends. When your investments pay dividends, buying more shares rather than spending them extends the compounding chain. Index funds that automatically reinvest dividends have historically outperformed those that pay out cash, purely through the mechanics of compound interest on additional shares.

Fourth, eliminate high-interest debt aggressively. Credit card balances at 20%+ APR represent compound interest working against you at maximum speed. Paying minimum payments on $10,000 at 24% can take decades to clear while paying thousands in interest. Prioritize eliminating this debt before building investments, because guaranteed 24% “returns” from elimination exceed any plausible investment returns.

Fifth, use tax-advantaged accounts. Compound interest operates on after-tax dollars in regular accounts. In Roth IRAs and 401(k)s, it operates on pre-tax dollars, dramatically accelerating growth. The tax treatment doesn’t change the compound formula, but it changes what’s being compounded—gross versus net contributions.

The Uncomfortable Truth About Waiting

You will not find this in most compound interest articles, but it needs saying: telling someone “just start investing” without addressing why they aren’t already investing is incomplete advice.

Most people who don’t invest aren’t avoiding it out of ignorance. They’re avoiding it because they can’t afford to. Median savings in America hovers around $5,000—nowhere near enough to weather a $1,000 emergency without credit card debt. Asking someone earning $40,000 annually with $12,000 in high-interest credit card debt to start compounding ignores their actual constraints.

Compound interest is real. Its power is real. But it applies most powerfully to those who already have financial breathing room. If you’re drowning in debt or living paycheck to paycheck, the immediate priority is building an emergency fund and eliminating high-interest balances—not pursuing investment returns that might take a decade to materialize.

This doesn’t mean compound interest isn’t for you. It means the sequence matters. Stabilize your financial foundation first. Then let compound interest do what it does best—work quietly in the background, year after year, turning consistency into规模.

The eighth wonder of the world doesn’t require believing in magic. It requires believing in mathematics—and then giving that mathematics time to work.