Every serious investor needs a working knowledge of financial statements, and the profit and loss statement—often called the income statement or P&L—is fundamental to that foundation. Yet plenty of investors can recite stock prices from memory but glaze over when confronted with a company’s earnings report. That’s a real problem. The P&L tells you whether a business is actually making money, how it’s making that money, and whether those profits are growing or shrinking. Ignore it, and you’re investing blind.

This guide walks you through interpreting a P&L statement. You’ll learn what each line item means, how to spot the numbers that actually matter, and where conventional wisdom about reading earnings reports leads investors astray. By the end, you’ll be able to look at any company’s income statement and extract the story underneath the numbers.

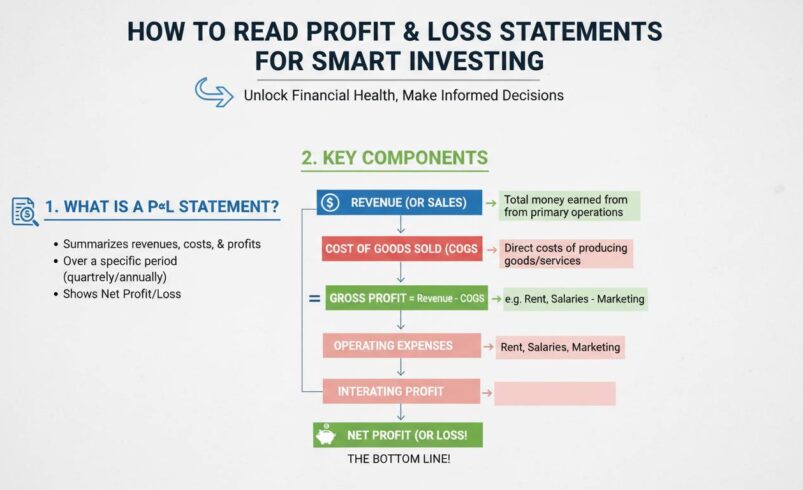

What a Profit and Loss Statement Actually Shows

A profit and loss statement summarizes a company’s revenues and expenses over a specific period—typically a quarter or a full fiscal year. Think of it as a video rather than a photograph: it captures financial performance over time, not a single moment like the balance sheet does.

The basic equation is simple: Revenue minus Expenses equals Profit (or Loss). But the P&L breaks this into several layers, each revealing something different about the business. Revenue represents the total money coming in from sales. Expenses get categorized by type—some directly tied to producing goods or services, others related to running the company overall. The final line, net income, shows what’s left after everything gets accounted for.

For investors, the P&L answers the core questions: whether the company is growing, whether it’s efficient, and whether its profits are real—meaning they reflect actual cash earned, not just accounting adjustments.

The Key Components of Any P&L Statement

Every income statement follows a roughly similar structure, though line items vary by industry. Here’s what you need to understand.

Revenue (or Sales/Net Sales)

This sits at the top of the statement. Revenue represents the total inflow from primary business activities—products sold, services rendered, subscriptions collected. A company might have other income sources (interest, asset sales), but revenue from core operations is what matters most for evaluating the business itself.

When analyzing revenue, investors should look for consistency and growth. Amazon’s AWS revenue, for instance, has shown strong year-over-year growth, while its retail revenue growth has fluctuated more dramatically. Context matters. A 10% revenue increase means something different for a mature utility company than for a fast-growing software startup.

Cost of Goods Sold (COGS)

COGS captures the direct costs of producing whatever the company sells. For a manufacturer, this includes raw materials and direct labor. For a retailer, it’s what they paid for inventory. For a software company, COGS might include hosting costs and customer support.

The relationship between revenue and COGS produces one of the most important numbers on the entire statement: gross profit.

Gross Profit and Gross Margin

Gross profit equals revenue minus COGS. Gross margin expresses this as a percentage of revenue. If a company has $1 million in revenue and $400,000 in COGS, gross profit is $600,000 and gross margin is 60%.

Margins matter for comparative analysis. A grocery store might operate on 25% gross margins, while a software company could see 70% or higher. What constitutes a “good” margin depends entirely on the industry. Comparing a pharmaceutical company’s margins to a grocery chain’s tells you nothing useful.

One thing to watch: companies have some flexibility in how they classify costs between COGS and operating expenses. This means gross margins aren’t always perfectly comparable between companies, even in the same industry. Always check the footnotes to see exactly what’s included in COGS.

Operating Expenses

Operating expenses cover everything needed to run the company that isn’t directly tied to production. Common categories include:

- Selling, General, and Administrative (SG&A): Marketing, salaries for non-production staff, rent, utilities

- Research and Development (R&D): Especially important for tech and pharmaceutical companies

- Depreciation and Amortization: Non-cash charges reflecting the gradual wear-down of assets

Operating income—sometimes called earnings before interest and taxes (EBIT)—is what remains after subtracting operating expenses from gross profit. This number tells you how profitably the core business operates, separate from financing decisions and tax situations.

Net Income

The bottom line. Net income accounts for interest expenses, taxes, and any one-time items or discontinued operations. It’s the profit theoretically available for distribution to shareholders (though companies often retain it rather than paying it out).

Here’s an uncomfortable truth many investors overlook: net income is the most manipulated number on the entire statement. Executives have considerable discretion over timing of expenses, revenue recognition, and reserves. That’s not necessarily fraud—it’s often legitimate accounting judgment—but it means you shouldn’t take net income at face value without understanding what drives it.

Reading a P&L Statement in Practice

Theory only gets you so far. Let’s walk through a simplified example to see how these components interact.

Consider a hypothetical retail company with the following P&L for 2024:

| Line Item | Amount |

|---|---|

| Revenue | $10,000,000 |

| Cost of Goods Sold | $6,000,000 |

| Gross Profit | $4,000,000 (40% margin) |

| Operating Expenses | $2,500,000 |

| Operating Income | $1,500,000 |

| Interest Expense | $200,000 |

| Taxes | $350,000 |

| Net Income | $950,000 |

From this, you can immediately see several things. The 40% gross margin tells you about pricing power and cost structure. Operating expenses consuming 25% of revenue ($2.5M / $10M) indicates operational efficiency. Net income of $950,000 on $10 million in revenue produces a 9.5% profit margin—reasonable for retail but nothing extraordinary.

Now imagine the 2025 statement shows revenue up 15% to $11.5 million. Sounds great, right? But if COGS rose to $8 million (nearly 70% of revenue) due to supply chain problems, gross profit actually dropped to $3.5 million despite higher sales. That inverted story is exactly what reading a P&L line-by-line reveals.

What Smart Investors Actually Look For

Knowing the components isn’t enough. You need a framework for evaluating what you see.

Revenue Growth Trends

Don’t just look at one year. Revenue growth should be analyzed over multiple periods—quarter-over-quarter and year-over-year. A company might show strong annual growth but reveal concerning deceleration when you examine sequential quarters.

Consider Apple. In recent years, total revenue growth has been modest (often low single digits), but services revenue has grown much faster. An investor looking only at aggregate revenue would miss this important shift in business composition.

Profit Margins Across the Income Statement

I already mentioned gross margin and net margin, but there are others. Operating margin (operating income as a percentage of revenue) deserves particular attention. It shows profitability from core operations before financing and taxes distort the picture.

Healthy companies typically show improving margins over time. If revenue grows faster than expenses, margins expand—a phenomenon called operating leverage. When expenses grow faster than revenue, margins compress—a warning sign. Many unprofitable growth companies argue that margins will improve once they achieve scale. Sometimes that’s true; often it isn’t. Always verify the logic.

The Relationship Between Net Income and Cash Flow

This is where many retail investors get tripped up. Net income follows accrual accounting, which records transactions when they happen—not when cash changes hands. A company can show profit on the P&L while actually burning cash.

Amazon provides a useful example. For years, the company reported minimal net income (or even losses) while generating substantial cash flow from operations. Investors who focused only on net income completely missed the story. That’s why you should always compare net income to cash flow from operations on the cash flow statement. Significant divergence warrants investigation.

One-Time Items and Adjustments

Companies frequently report “pro forma” or “adjusted” earnings that exclude certain charges. Stock-based compensation, restructuring costs, acquisition-related expenses, and asset impairments often get stripped out. Sometimes this makes sense for understanding underlying performance. Other times, it’s sleight of hand.

Ask yourself: if you add back all the “one-time” items the company excluded, what’s the actual earnings picture? If they’re consistently excluding the same categories year after year, those aren’t one-time items—they’re part of how the business runs.

Essential Terms Every Investor Should Know

Certain terms appear frequently in earnings reports and financial discussions. Adding these to your vocabulary sharpens your analysis.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): A proxy for operating cash flow that strips out financing decisions and non-cash charges. Useful for comparing companies with different capital structures, though it’s not a real cash number and gets abused by some managements.

EBIT: Earnings before interest and taxes—essentially operating income. Simpler and more standardized than EBITDA.

EPS (Earnings Per Share): Net income divided by shares outstanding. The number most directly affects stock price since it tells you how much profit belongs to each share. Investors should understand how share count changes (dilution) affect EPS.

Operating Leverage: The degree to which a company’s costs are fixed versus variable. High operating leverage means small revenue changes produce large profit changes—both positive and negative.

Revenue Recognition: The accounting principle determining when revenue gets recorded. This has been a frequent source of accounting scandals because companies can manipulate timing. SaaS companies, for instance, recognize subscription revenue over the contract period, not when cash is collected.

Where P&L Statements Fall Short

Here’s something the finance world doesn’t discuss enough: the income statement has significant blind spots. Understanding these limitations prevents you from overrelying on P&L analysis.

The P&L ignores working capital changes. A company can report profits while simultaneously running out of cash if receivables swell and inventory piles up. That’s why the cash flow statement exists—and why you should never analyze a P&L in isolation.

It reflects historical performance. By the time quarterly earnings are released, the information is weeks or months old. Markets are forward-looking; your analysis should be too.

Management has considerable accounting discretion. From revenue recognition timing to depreciation assumptions to reserve building, numbers on the P&L reflect choices management made. Those choices might be entirely reasonable—or they might be designed to paint the rosiest picture possible.

Non-GAAP metrics lack standardization. When companies report “adjusted” or “pro forma” earnings, they’re essentially inventing their own profit measure. One company’s “adjusted EBITDA” might exclude items that another’s includes. Always reconcile to GAAP net income to understand what’s really happening.

The P&L doesn’t show the full picture of value creation. A company can generate profits while destroying shareholder value if its cost of capital exceeds its returns. Return on invested capital (ROIC) captures this; net income alone does not.

Bringing It All Together

Reading a P&L statement isn’t about memorizing formulas—it’s about developing judgment. Start with revenue to understand the top-line growth story. Move to gross margin to assess fundamental economics. Examine operating expenses relative to revenue for efficiency clues. Finally, arrive at net income with appropriate skepticism, always comparing it to cash flow and checking what adjustments management made.

The best investors treat financial statements as a story in numbers. The P&L tells you about profitability. The balance sheet shows what the company owns and owes. The cash flow statement reveals whether the profits are real. Together, they form a complete picture that no single number could provide.

No article can make you an expert analyst—that takes years of practice and thousands of hours reading filings. But understanding the P&L removes one of the biggest barriers to serious investing. You’re no longer dependent on headline numbers or what someone on television says a company “earned.” You can look yourself, form your own conclusions, and invest with genuine conviction.

The financial statements are there for everyone to read. Most investors never bother. If you take the time to learn, you’re already ahead of most people in the market.